Question

Answer

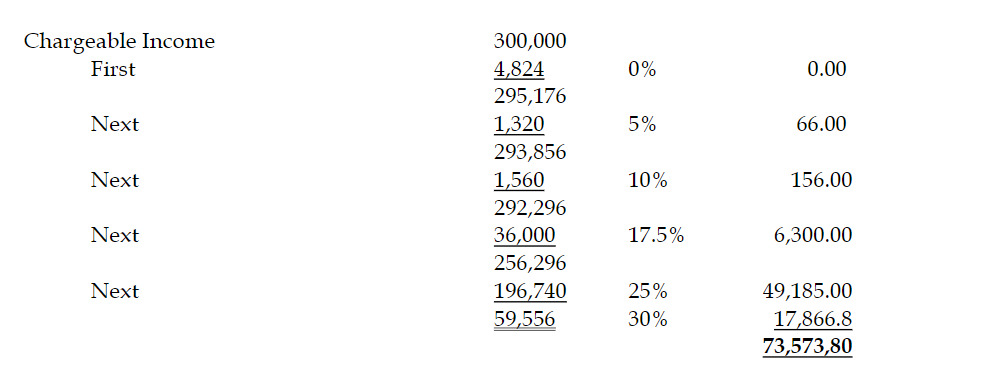

Computation of tax payable – Mr Agandi

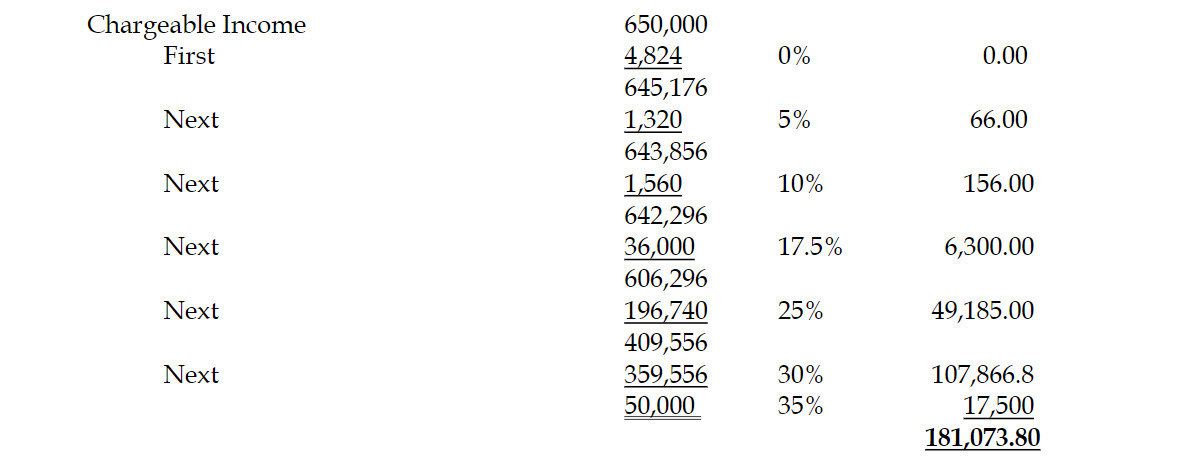

Computation of tax payable – Mr Yonny

Non-Residents

The chargeable income of non-resident individuals is taxed at a flat rate of 25%.

Tax Payable Mrs. Zindana: 25% x 300,000 = GH¢75,000

Tax Payable Mrs. Maleda: 25% x 650,000 = GH¢162,500