Question

Answer

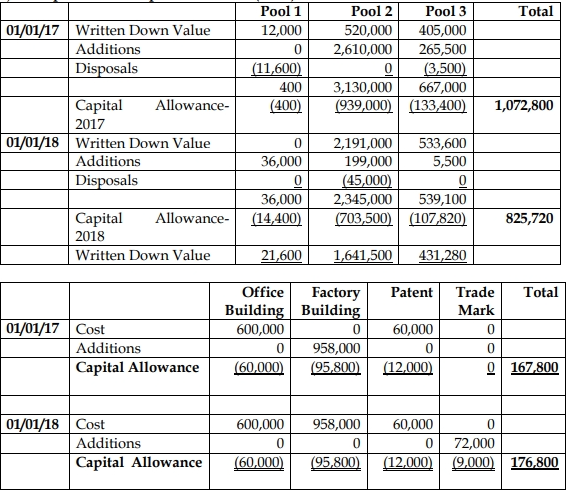

a) Computation of Capital allowance (GH¢)

b) Explanation of the Class or Pool System

- The pool system groups depreciable assets of the same class for capital allowance computation.

- In this system, the identity of individual assets is lost as they are aggregated into pools.

- Class 1 to 3 assets follow the pool system, while Class 4 and 5 assets (such as buildings and intangibles) are kept separately for each item.

- Assets in a pool receive capital allowances based on the written-down value (WDV) of the pool.

- Assets used solely for income production are placed in the pool, and any disposals reduce the pool value.