Question

Kologo Municipal Hospital is a Public Hospital established in the Upper East Region, which serves several communities. Its Trial Balance for the year ended 31 December 2020 is provided below.

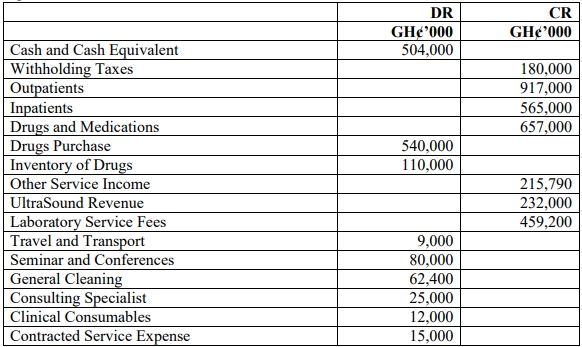

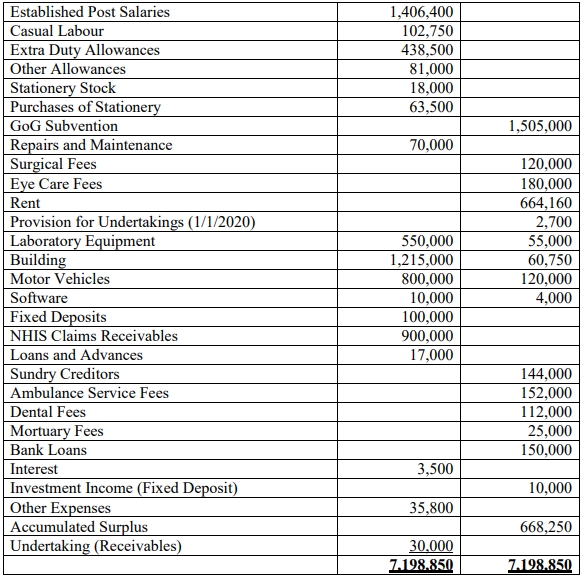

Trial Balance as at 31 December 2020

Additional Information

i) The hospital’s policy is to apply the Accrual Basis of Accounting in preparing its Financial Statements in compliance with the Public Financial Management Act, 2016 (Act 921), Public Financial Management Regulation 2019 L.I 2378, and the International Public Sector Accounting Standards (IPSAS).

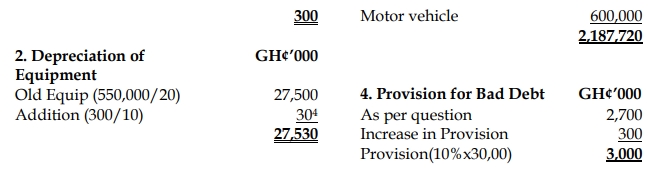

ii) The hospital purchased equipment at the cost of GH¢200,000 on 1 April 2020.

iii) A new equipment valuing GH¢100,000 was donated to the hospital on 1 July 2020. The equipment was assessed to have a useful life of ten (10) years. This has not yet been accounted for in the Trial Balance.

iv) The Fixed Deposit attracts an interest of 15% per annum.

v) Inventory of drugs as at 31 December 2020 amounted to GH¢95,000,000 at cost and had a net realizable value of GH¢110,000,000 but its replacement cost is GH¢78,000,000. In addition, stationery stock as at 31 December 2020 cost GH¢28,000,000 and has a replacement cost of GH¢25,000,000 with an estimated net realizable value of GH¢35,000,000.

vi) Redundancy pay outstanding as at the end of the year amounted to GH¢25,950,000.

vii) Provision for undertaking is estimated at 10%.

viii) The hospital currently owes Healer Pharmaceuticals for Drugs amounting to GH¢1,950,000 supplied to the hospital during the years 2020 and 2021 in respect of the following months:

- November 2020: GH¢820,000

- December 2020: GH¢610,000

- January 2021: GH¢520,000

- Totals: GH¢1,950,000

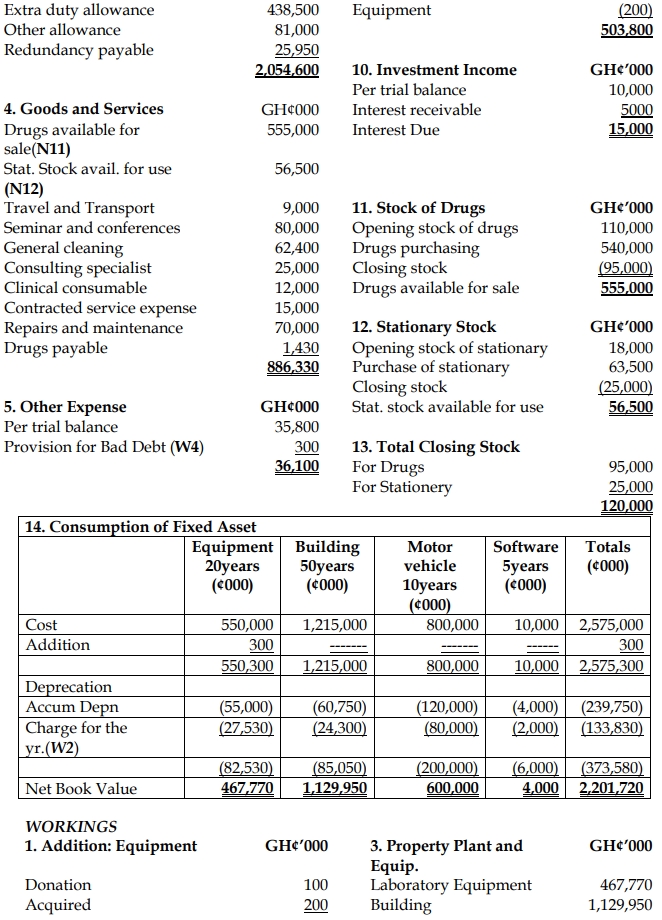

ix) Consumption of Fixed Assets is charged on a straight-line basis with time apportionment in the year of acquisition.

- Asset | Useful life

- Laboratory Equipment | 20 years

- Building | 50 years

- Motor Vehicles | 10 years

- Software | 5 years

Required:

Prepare in compliance with the IPSAS and relevant legislation:

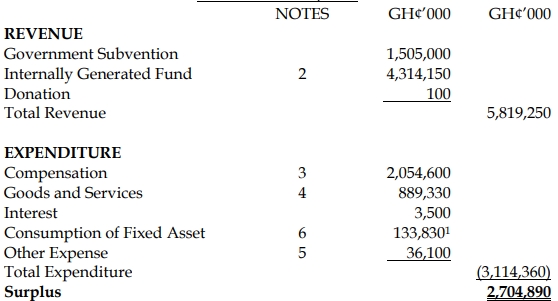

a) Statement of Financial Performance for the year ended 31 December 2020.

(8 marks)

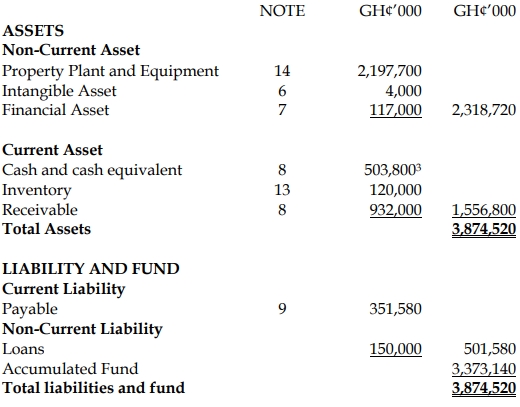

b) Statement of Financial Position as at 31 December 2020.

(8 marks)

c) Notes to the Accounts.

(4 marks)

Answer

Statement of Financial Performance for the year ended 31 December 2020

Statement of Financial Position as at 31 December 2020

b) Statement of Financial Position as at 31 December 2020.

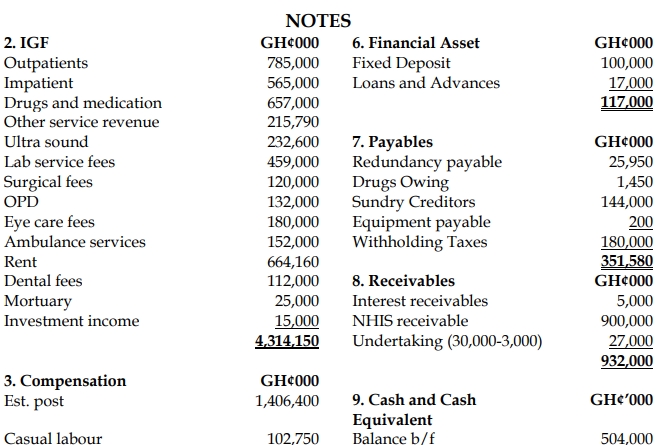

Notes to the Financial Statements

- Significant accounting policies applied for the preparation of the financial statements include the following:

- Compliance with IPSAS and PFM Act.

- The financial statements have been prepared in conformity with the Financial Management Act, 2016(Act 921), Public Financial Management Regulation 2019 L.I 2378 and the International Public Sector Accounting Standards (IPSAS).

- Basis of accounting.

The financial statements have been prepared on an accrual basis where transactions and events are recognised as and when they occur. - Cost measurement.

Assets are measured on a historical cost basis except for motor vehicle donated to the assembly, which was measured and recognised at fair value. - Consumption of fixed assets.

Consumption of fixed assets are charges using a straight-line basis. The estimated useful life of the assets are as follows:

Laboratory Equipment 20 years

Building 50years

Motor Vehicles 10 years

Software 5years - Valuation of inventory.

Inventory of office consumables was valued at lower of cost and current replacement cost in compliance with IPSAS 12: inventory