Question

Answer

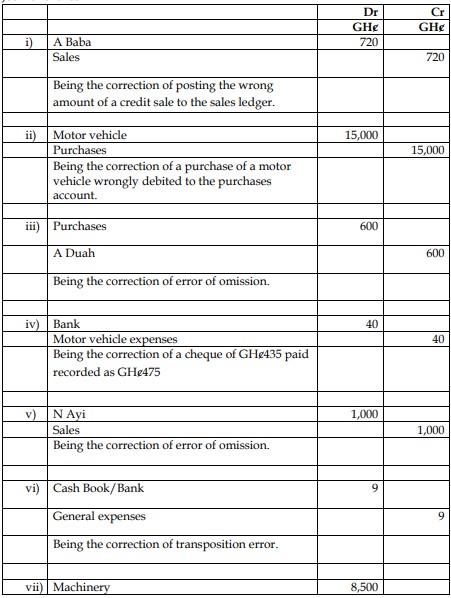

a) Journal Entries

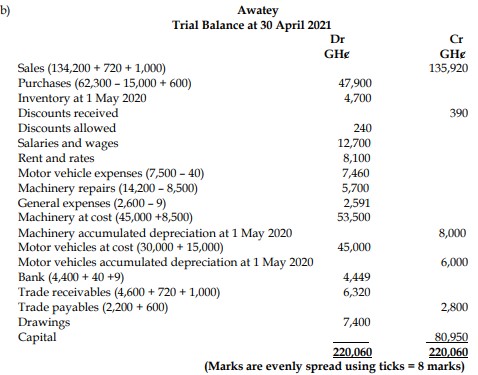

c)

Types of Errors Not Affecting Trial Balance

- Error of Omission:

When a transaction is completely omitted from the books, neither a debit nor a credit entry is made, and thus the trial balance remains balanced. - Error of Principle:

This occurs when a transaction is entered in the wrong class of account. For example, treating a capital expenditure as revenue expenditure. The trial balance will still balance because the double entry is correctly recorded, but the transaction is misclassified.

(4 marks evenly spread)