Question

Biggs Ltd has a financial year ending 31 December. Its trial balance extracted as at 31 December 2018 is as follows:

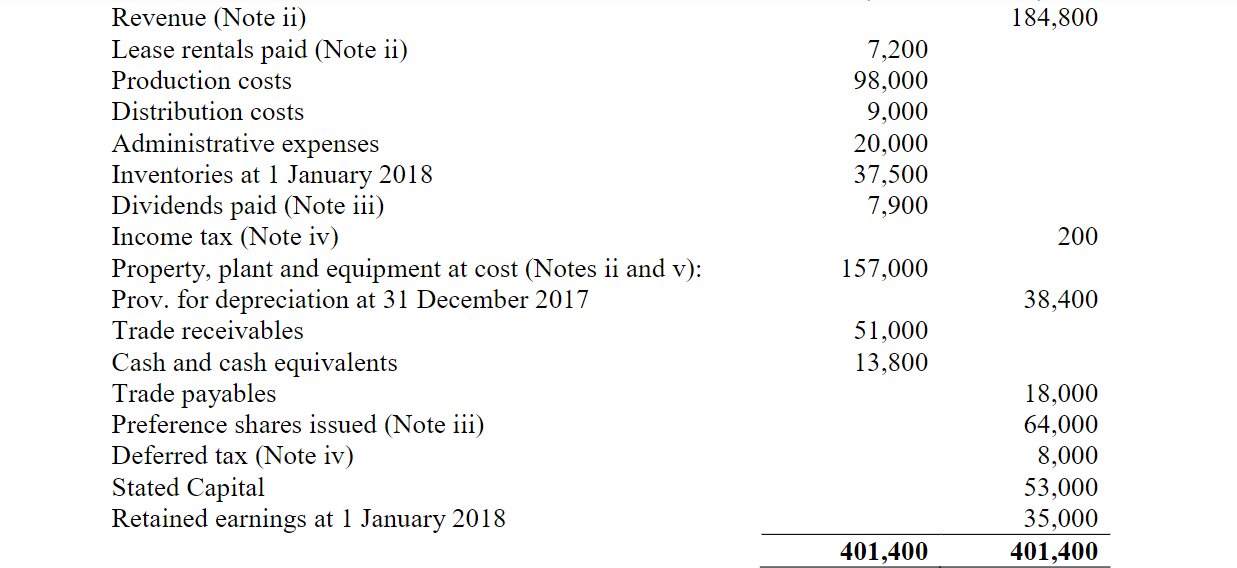

![]()

Additional Information:

i) The carrying value of inventories at cost at 31 December 2018 was GH¢39.5 million.

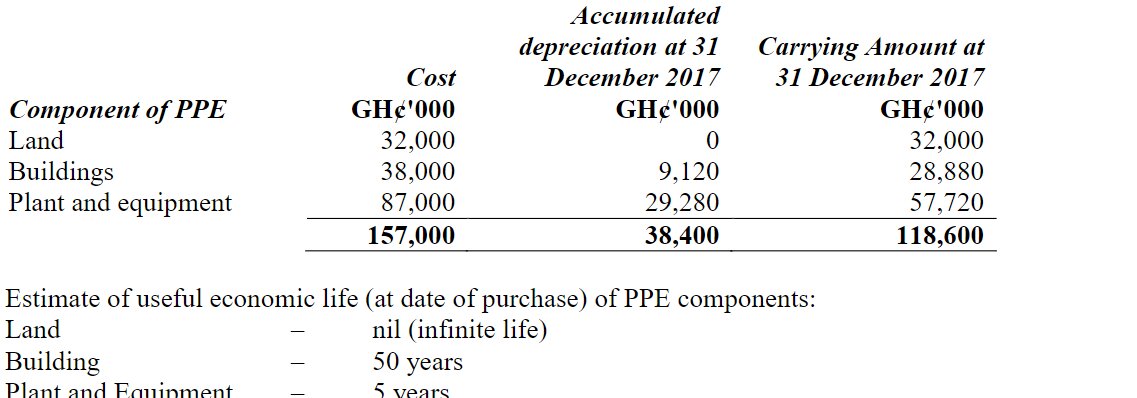

The estimated useful life (at the date of purchase) of the PPE components is:

- Land: infinite life

- Buildings: 50 years

- Plant and equipment: 5 years

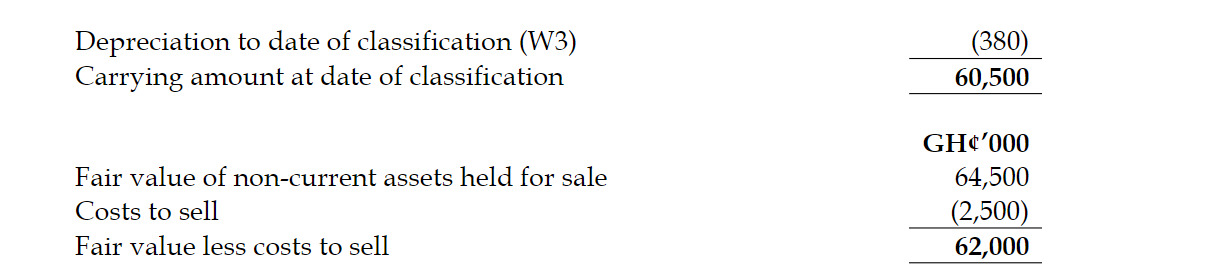

On 30 June 2018, the directors decided to sell the property because more suitable leasehold property had become available at a very competitive cost. They advertised the property for sale at that date at what was considered to be a realistic asking price of GH¢68 million. They estimated that costs of GH¢3 million would be necessary in order to sell the property. On 1 December 2018, they reduced the asking price to GH¢64.5 million and sold the property at this price shortly after the year-end. Costs to sell totaled GH¢2.5 million.

Required:

Prepare for Biggs Ltd:

a) The Statement of Profit or Loss and Other Comprehensive Income for the year ended 31 December 2018. (10 marks)

b) The Statement of Financial Position as at 31 December 2018. (10 marks)

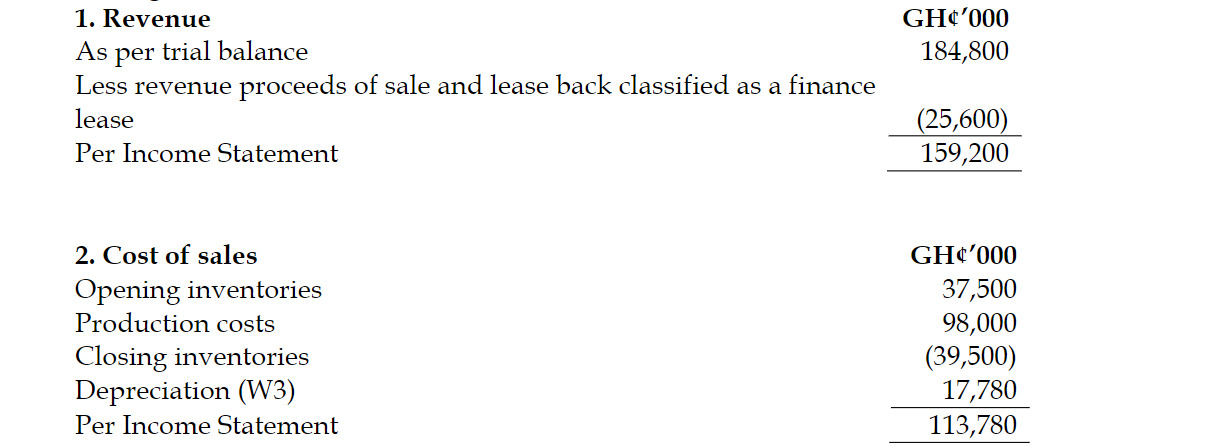

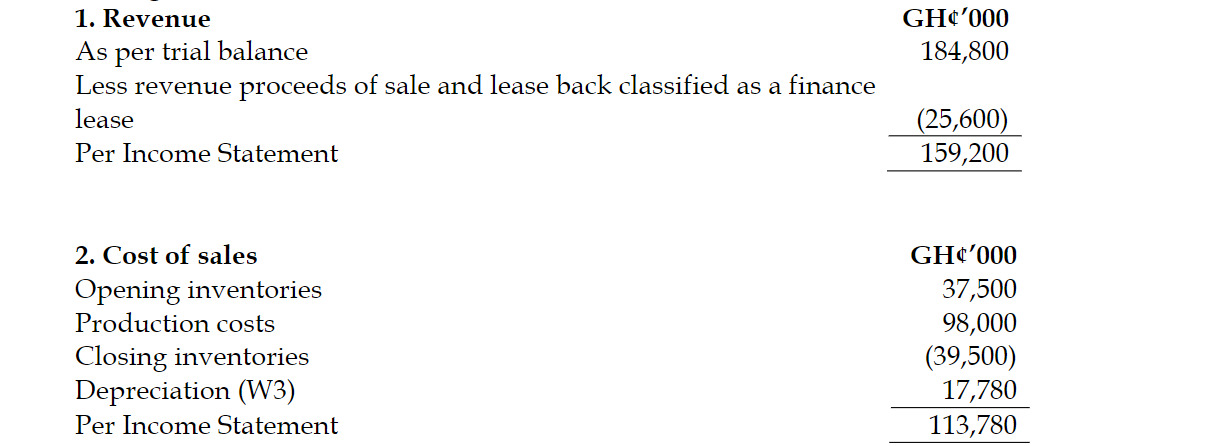

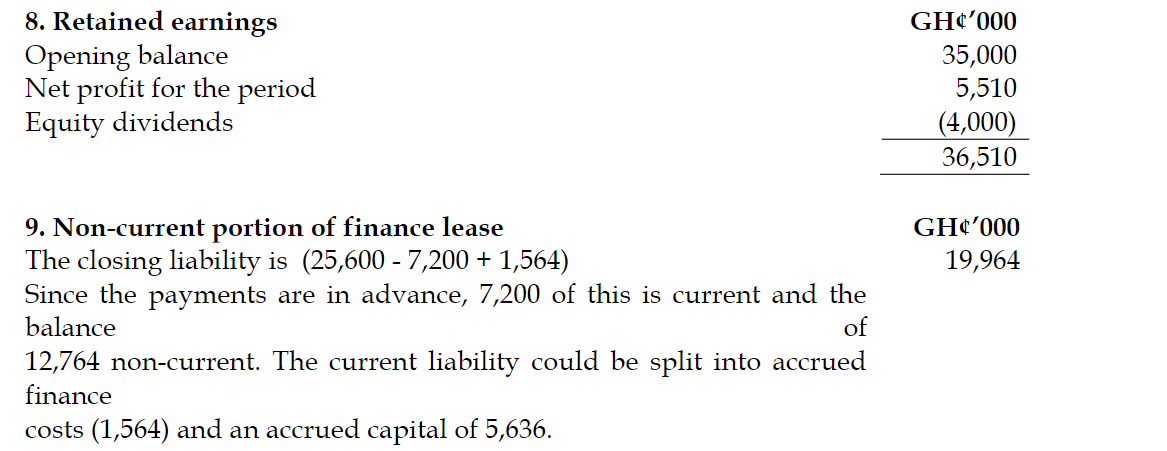

ii) On 1 January 2018, Biggs Ltd sold some of its plant and equipment to a finance company. Biggs Ltd credited the sales proceeds of GH¢25.6 million to revenue. The plant and equipment were purchased by Biggs Ltd on 1 January 2017 at a total cost of GH¢32 million and were being depreciated over five years. The cost and accumulated depreciation of the disposed asset are still included in the PPE cost and accumulated depreciation accounts.

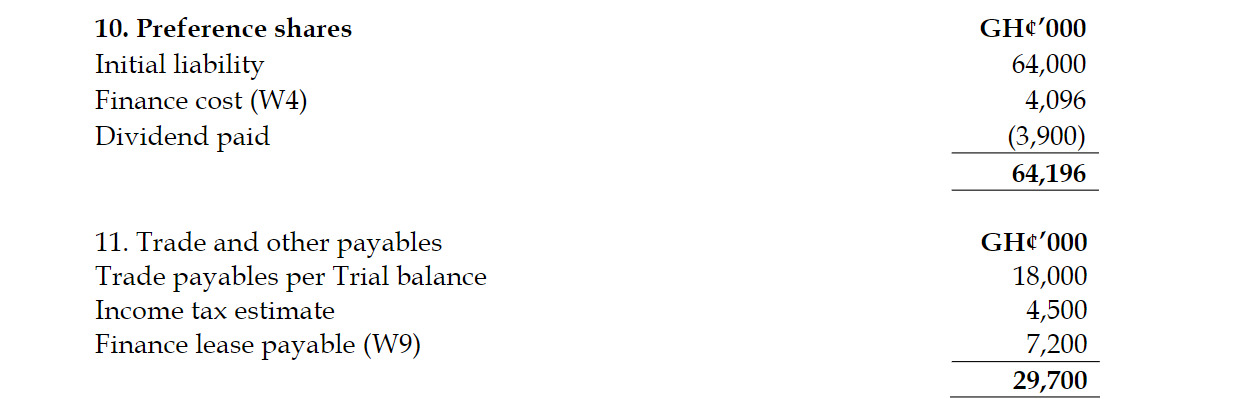

iii) On 1 January 2018, Biggs Ltd issued 200 million preference shares at 32.50 pesewas each. Costs of issue were GH¢1 million so the net proceeds of the issue were GH¢64 million. The preference shareholders will receive an annual dividend on 31 December each year of GH¢3.9 million. The shares will be redeemed at par on 31 December 2022. The effective annual finance cost attached to these shares is approximately 6.4%. The first annual dividend was paid on 31 December 2018 and is included in dividends paid.

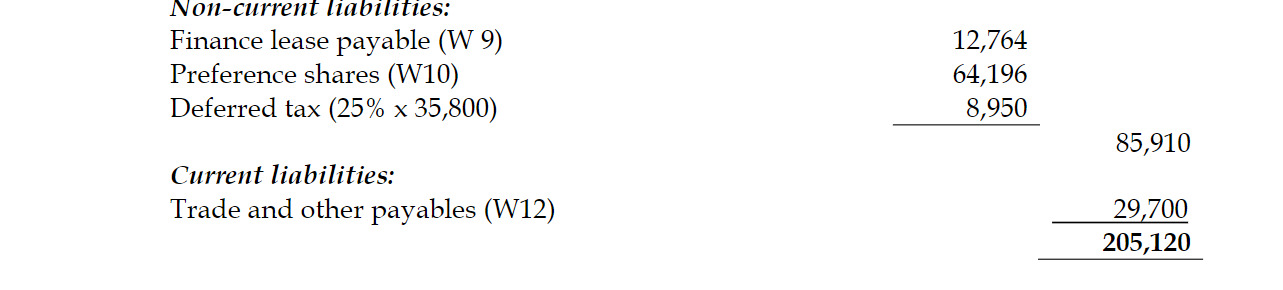

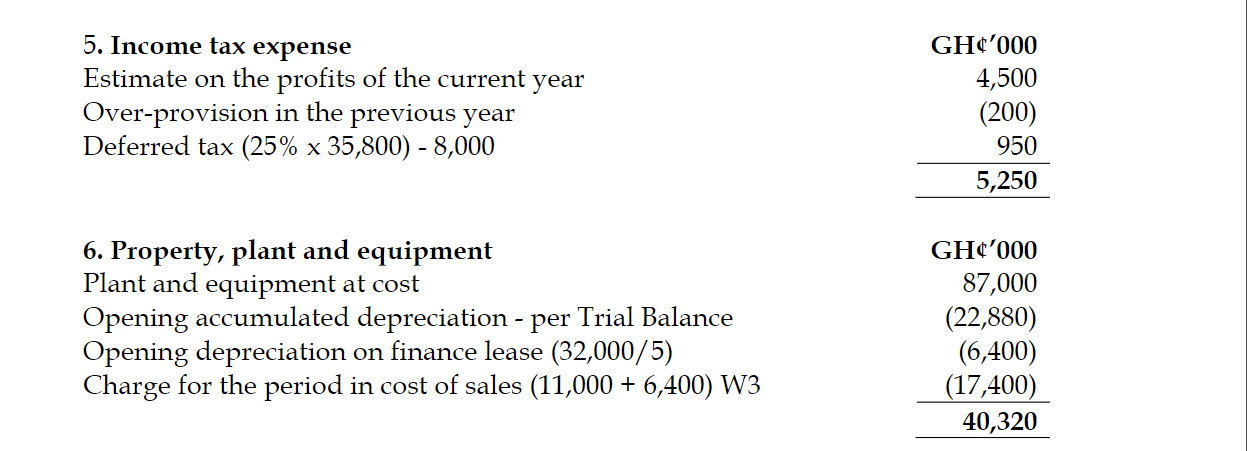

iv) The estimated income tax on the profits for the year to 31 December 2018 is GH¢4.5 million. During the year GH¢4.2 million was paid in full and final settlement of income tax on the profits for the year ended 31 December 2017. The statement of financial position at 31 December 2017 had included GH¢4.4 million in respect of this liability. At 31 December 2018, the carrying amounts of the net assets of Biggs Ltd exceeded their tax base by GH¢35.8 million. Assume an income tax rate of 25%.

v) The details of property, plant, and equipment are as follows:

Answer

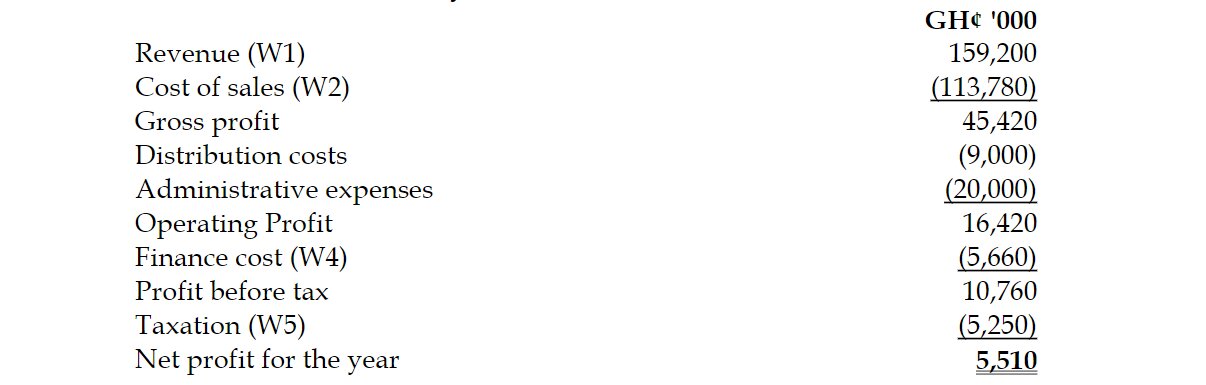

Biggs Ltd

Statement of Profit or Loss

For the year ended 31 December 2018

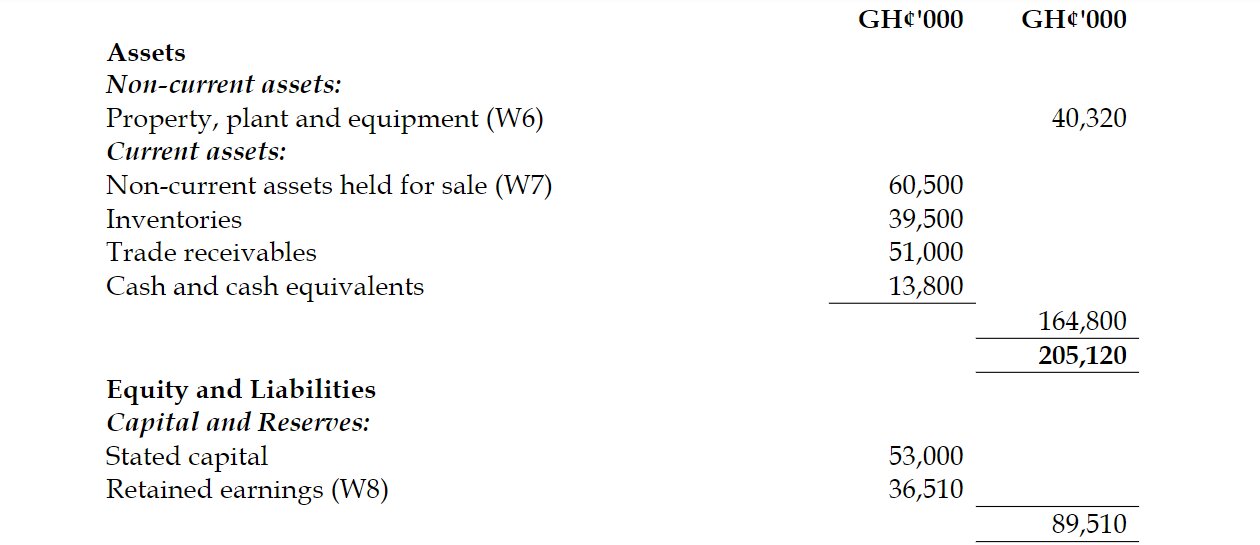

Biggs Ltd

Statement of Financial Position as at 31 December 2018

Workings

NB: Since the carrying amount is less than the fair value less cost to sell, the non-

current assets held for sale would be included in the statement of financial position at

the carrying amount.

(80 ticks @ 0.25 marks per tick for all components of the question)