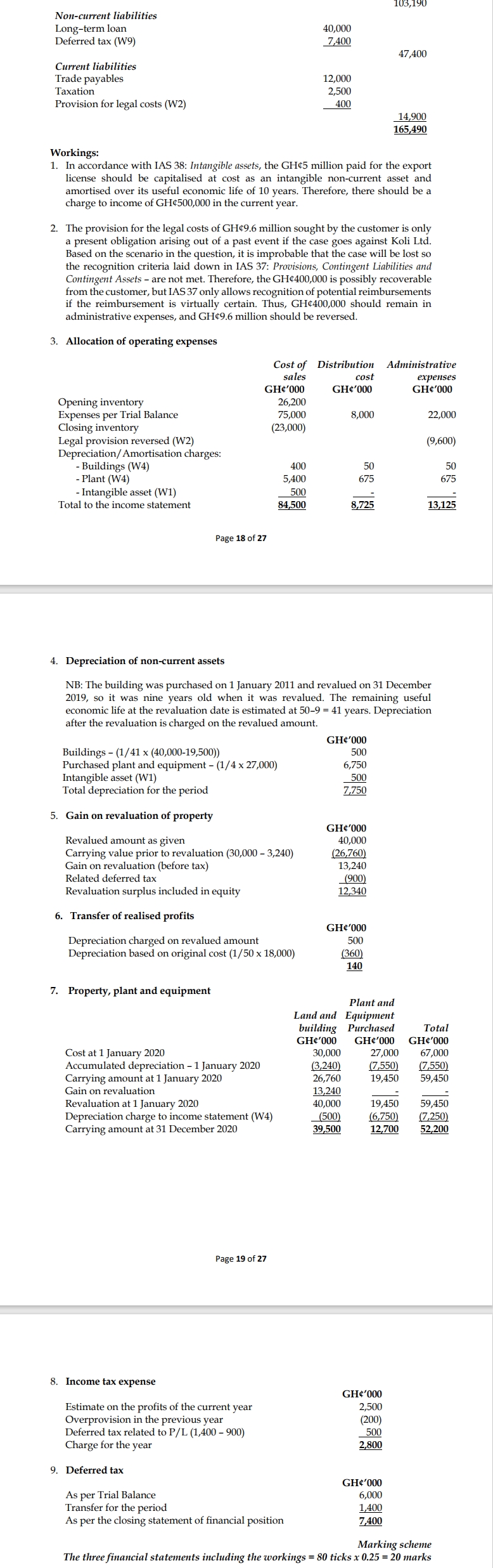

- 20 Marks

Question

The following trial balance relates to Koli Ltd for the year ended 31 December, 2020.

| Description | Debit (GH¢’000) | Credit (GH¢’000) |

|---|---|---|

| Sales | 128,000 | |

| Purchases | 75,000 | |

| Distribution expenses | 8,000 | |

| Administrative expenses (Note ii) | 22,000 | |

| License (Note iii) | 5,000 | |

| Inventories at 31 December 2019 | 26,200 | |

| Finance costs on a long-term loan | 3,000 | |

| Income tax (Note iv) | 200 | |

| Deferred tax (Note iv) | 6,000 | |

| Dividend paid on equity shares | 2,000 | |

| Property, Plant and Equipment (PPE) | 57,000 | |

| Provision for depreciation on PPE | 10,790 | |

| Trade receivables | 52,000 | |

| Bank balances | 33,790 | |

| Trade payables | 12,000 | |

| Provision for legal costs (Note ii) | 10,000 | |

| Long-term loan | 40,000 | |

| Stated capital | 50,000 | |

| Retained earnings as at 31 December 2019 | 27,000 | |

| Total | 283,990 | 283,990 |

Additional information:

i) The carrying value of inventories on 31 December 2020 was GH¢23 million.

ii) Administrative expenses include a provision of GH¢10 million for the possible costs of a legal claim lodged against Koli Ltd by one of its customers before 31 December 2020. The directors of Koli Ltd consider that it is probable that Koli Ltd can successfully defend the case, but they are providing for the worst possible outcome on the grounds of prudence. The provision of GH¢10 million is for the amount sought by the customer (GH¢9.6 million) plus the directors’ best estimate of the legal costs incurred in defending the case.

iii) On 1 January, 2020, Koli Ltd paid GH¢5 million for a ten-year export license.

iv) The estimated income tax on the profits for the year to 31 December 2020 is GH¢2.5 million. During the year, GH¢2.2 million was paid in full and in the final settlement of income tax on the profits for the year ended 31 December 2019. The statement of financial position on 31 December 2019 had included GH¢2.4 million in respect of this tax liability. A transfer of GH¢1.4 million is required to increase the deferred tax liability in the statement of financial position; GH¢900,000 of this amount was necessary due to the taxable temporary difference caused by the property revaluation (see note v below).

v) The details of property, plant and equipment are as follows:

| Component of PPE | Cost (GH¢’000) | Accumulated Depreciation (GH¢’000) | Carrying Amount (GH¢’000) |

|---|---|---|---|

| Land | 12,000 | 0 | 12,000 |

| Buildings | 18,000 | 3,240 | 14,760 |

| Plant and Equipment | 27,000 | 7,550 | 19,450 |

| Total | 57,000 | 10,790 | 46,210 |

Estimate of useful economic life (at the date of purchase) of PPE components:

- Land: nil (infinite life)

- Building: 50 years

- Plant and Equipment: 4 years

Depreciation of property, plant and equipment is allocated as follows:

- 80% to cost of sales

- 10% to distribution expenses

- 10% to administrative expenses

On 1 January, 2020, the directors of Koli Ltd decided to revalue its property (Land and Building) to its market value of GH¢40 million, including GH¢19.5 million for the Land. The original estimate of the useful economic life of the property was still considered valid. The directors wish to make an annual transfer of excess depreciation from the revaluation reserve to realized profits following the revaluation.

Required:

Prepare for Koli Ltd,

a) The Statement of Profit or Loss and Other Comprehensive Income for the year ended 31 December 2020. (8 marks)

b) The Statement of Changes in Equity for the year ended 31 December 2020. (4 marks)

c) The Statement of Financial Position as at 31 December 2020. (8 marks)

(Total: 20 marks)

Answer

- Tags: Accounting Treatment, Financial Statements, Profit or Loss, Trial Balance

- Level: Level 2

- Topic: Preparation of Financial Statements

- Series: MAY 2021

- Uploader: Olaoluwa