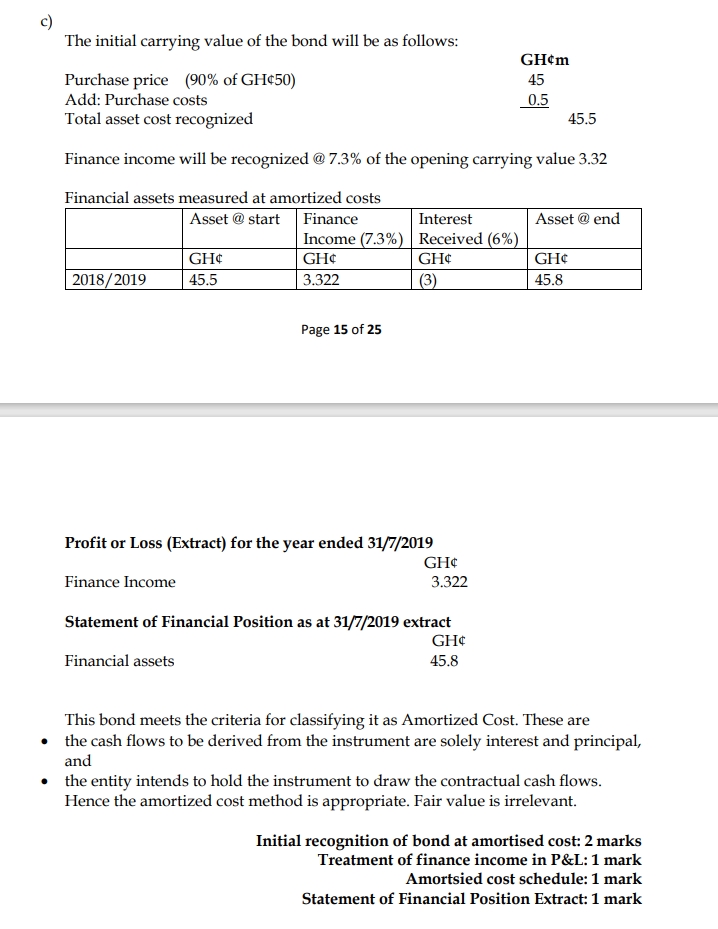

Asamankese Ltd (Asamankese) purchased a 6% GH¢50 million bond on 1 August 2018 at a 10% discount to par value. Expenses of purchase were GH¢500,000. The bond is due for redemption on 31 July 2028 at par. The effective annual interest rate to maturity is 7.3%. Asamankese intends to hold the bond until its maturity date.

Required:

In accordance with IFRS 9: Financial Instruments, how much should be recognized in Asamankese’s financial statements in respect of the above transaction for the year ended 31 July 2019 (to two decimal places)?