Question

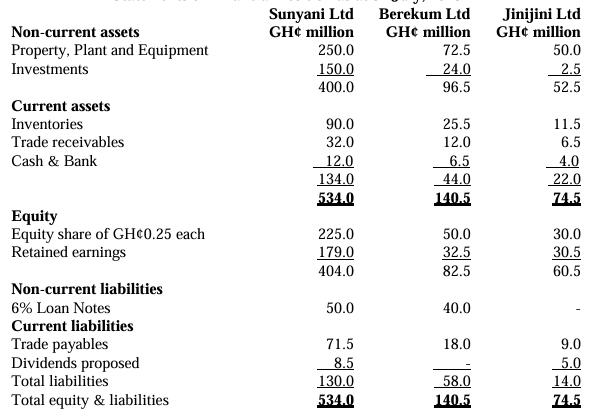

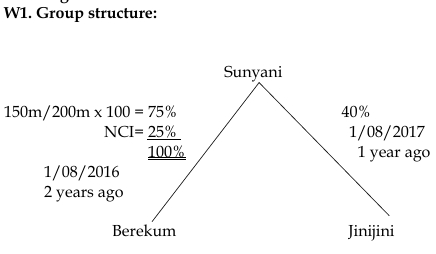

Sunyani Ltd (Sunyani) is a limited liability company based in Brong Ahafo. It has shareholdings in two other companies, Berekum Ltd (Berekum) and Jinijini Ltd (Jinijini). Sunyani bought 150 million ordinary shares in Berekum on 1 August 2016, when the retained earnings of Berekum were GH¢22 million. The consideration was agreed at GH¢110 million for these shares.

On 1 August 2017, Sunyani bought a 40% holding in the ordinary shares of Jinijini when the retained earnings balance in Jinijini’s books stood at GH¢26 million. The consideration was an immediate cash payment of GH¢25 million. The directors of Sunyani negotiated the right to appoint 4 directors to Jinijini’s 12-person board as a result of its investment.

Statements of Financial Position are shown below for all three companies as at 31 July 2018.

Statements of Financial Position as at 31 July 2018:

Additional Information:

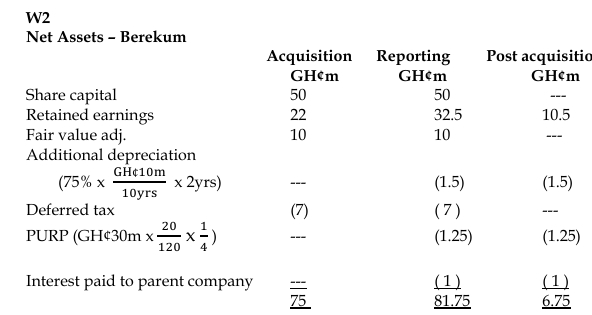

i) At the date of acquisition, Sunyani conducted a fair value exercise on Berekum’s net assets, which were equal to their carrying amounts with the following exceptions:

- A property held by Berekum had a fair value GH¢10 million in excess of its carrying value. 75% of the value of this property relates to buildings with a useful economic life of 10 years at the date of acquisition.

- Berekum had an unrecorded deferred tax liability of GH¢7 million, which was unchanged as at 31 July 2018.

ii) Sunyani’s policy is to value any Non-Controlling Interests (NCI) at their proportionate share of identifiable net assets at the acquisition date.

iii) Immediately after the acquisition, Berekum issued GH¢40 million of 6% loan notes, GH¢8 million of which were bought by Sunyani Ltd. This investment has been correctly recorded in the books of Sunyani under the heading “Investments.” All interest due on loan notes as at 31 July 2018 has been paid and recorded.

iv) During the financial year ended 31 July 2018, Berekum had sold goods to Sunyani amounting to GH¢30 million. The purchase price included a mark-up of 20% on cost. Berekum’s normal mark-up on goods sold is 60%. Of these goods, one-quarter remained in the closing inventory of Sunyani at the reporting date.

v) Sunyani has not accounted for any dividend receivable from its group companies. Both Sunyani and Jinijini have proposed dividends as shown in current liabilities. Jinijini’s proposed dividend relates entirely to the post acquisition period. No other dividends were paid or proposed in the year.

vi) Recorded in the books of Sunyani was an intra-group trade payable of GH¢10 million owed to Berekum at year-end. However, the books of Berekum showed a balance of GH¢11 million owed by Sunyani. It transpired that Berekum’s computer system had automatically charged to Sunyani’s account, interest of GH¢1 million due to late payments. It was subsequently agreed that Berekum would waive this interest.

vii) There were no impairment losses during the year end 31 July 2018.

(All workings may be rounded to the nearest GH¢0.01m)

Required: Prepare the Consolidated Statement of Financial Position for the Sunyani group as at 31 July 2018 in accordance with International Financial Reporting Standards.

Answer

Consolidated Statement of Financial Position for Sunyani Group Ltd as at 31 July 2018:

| GH¢ million | |

|---|---|

| Non-current assets | |

| Property, plant and equipment | 331 |

| Goodwill | 53.75 |

| Investment in Associate | 26.8 |

| Other investments | 31 |

| Total Non-current assets | 442.55 |

| Current assets | |

| Inventories | 114.25 |

| Trade receivables | 33 |

| Dividend receivable from Associate | 2 |

| Cash & Bank | 18.5 |

| Total Current assets | 167.75 |

| Total assets | 610.30 |

| Equity | |

| Equity shares | 225 |

| Retained earnings | 187.86 |

| Total Equity | 412.86 |

| Non-controlling interest | 20.44 |

| Total equity | 433.30 |

| Non-current liabilities | |

| 6% Loan note | 82 |

| Current liabilities | |

| Trade payables | 79.5 |

| Deferred tax liability | 7 |

| Dividends proposed | 8.5 |

| Total liabilities | 177 |

| Total equity & liabilities | 610.30 |

Workings:

Consolidated Statement of Financial Position for Sunyani Group Ltd as at 31 July 2018:

| GH¢ million | |

|---|---|

| Non-current assets | |

| Property, plant and equipment | 331 |

| Goodwill | 53.75 |

| Investment in Associate | 26.8 |

| Other investments | 31 |

| Total Non-current assets | 442.55 |

| Current assets | |

| Inventories | 114.25 |

| Trade receivables | 33 |

| Dividend receivable from Associate | 2 |

| Cash & Bank | 18.5 |

| Total Current assets | 167.75 |

| Total assets | 610.30 |

| Equity | |

| Equity shares | 225 |

| Retained earnings | 187.86 |

| Total Equity | 412.86 |

| Non-controlling interest | 20.44 |

| Total equity | 433.30 |

| Non-current liabilities | |

| 6% Loan note | 82 |

| Current liabilities | |

| Trade payables | 79.5 |

| Deferred tax liability | 7 |

| Dividends proposed | 8.5 |

| Total liabilities | 177 |

| Total equity & liabilities | 610.30 |

Workings:

- Depreciation on FV adjustment is calculated as:

- 75% of the property value (GH¢10 million) relates to buildings.

- Depreciation for 2 years: (GH¢10 million × 75%) ÷ 10 years = GH¢1.5 million.

W3: Goodwill – Proportionate Method

Goodwill is calculated using the proportionate share of net assets method:

- Cost of Investment in Berekum: GH¢110 million

- Share of Net Assets (75% of GH¢75 million): GH¢56.25 million

Goodwill = GH¢110 million – GH¢56.25 million = GH¢53.75 million

W4: Non-controlling Interest (NCI)

The NCI is valued at their proportionate share of identifiable net assets at the acquisition date.

NCI = 25% of GH¢81.75 million = GH¢20.44 million

W5: Group Retained Earnings

Calculation of the group’s retained earnings:

| Components | GH¢ million |

|---|---|

| Sunyani Ltd’s retained earnings | 179 |

| Share of post-acquisition profit from Associate Jinijini (40% of GH¢4.5 million) | 1.8 |

| Dividend Receivable from Associate Jinijini (40% of GH¢5 million) | 2 |

| Share of post-acquisition profit from Berekum (75% of GH¢6.75 million) | 5.06 |

| Total Group Retained Earnings | GH¢187.86 million |

W6: Investment in Associate (Jinijini Ltd)

Jinijini Ltd is treated as an associate, with significant influence due to a 40% shareholding.

| Components | GH¢ million |

|---|---|

| Cost of acquisition | 25 |

| Share of post-acquisition reserves (40% of GH¢4.5 million) | 1.8 |

| Total Investment in Associate | GH¢26.8 million |

W7: Fair Value Adjustments (Property)

At acquisition, Berekum had a property with a fair value GH¢10 million higher than its carrying value. This property includes buildings, depreciated over 10 years.

| Component | GH¢ million |

|---|---|

| At acquisition (FV adjustment) | 10 |

| Depreciation (75% of GH¢10 million over 2 years) | (1.5) |

| FV of Property | 8.5 million |

W8: Unrealised Profit on Intra-group Sales (PURP)

Berekum sold goods to Sunyani at a 20% mark-up. One-quarter of these goods were still in inventory at the reporting date.

- Goods in inventory: GH¢30 million × ¼ = GH¢7.5 million

- Profit on these goods: GH¢7.5 million × (20/120) = GH¢1.25 million

W9: Intra-group Payables and Interest

Sunyani owes Berekum GH¢10 million in trade payables. However, Berekum’s books show GH¢11 million due to a GH¢1 million interest charge, which was waived.

Adjustment:

- Eliminate the interest of GH¢1 million.

- Adjust both receivables and payables to reflect the correct intra-group balances.

W10: Dividends Receivable

Jinijini Ltd proposed a dividend of GH¢5 million, 40% of which is receivable by Sunyani.

Dividend Receivable = 40% of GH¢5 million = GH¢2 million

Conclusion:

This breakdown offers a comprehensive and clear explanation of the Consolidated Statement of Financial Position workings and their application in this financial reporting scenario.