Question

Answer

Zealow Ltd – Statement of Profit or Loss for the Year Ended 31 December 2015

| GH¢’000 | GH¢’000 |

|---|---|

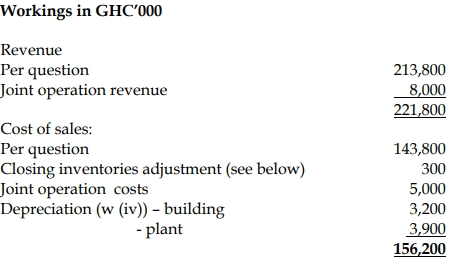

| Revenue (w(i)) | 221,800 |

| Cost of sales (w(i)) | (156,200) |

| Gross profit | 65,600 |

| Operating expenses | (22,400) |

| Investment income | 1,200 |

| Loss on investment property (16,000 – 13,500 w(ii)) | (2,500) |

| Financing cost (5,000 – 3,200 ordinary dividend (w(v))) | (1,800) |

| Profit before tax | 40,100 |

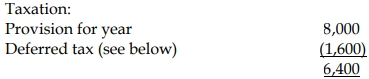

| Income tax expense (w(iii)) | (6,400) |

| Profit for the period | 33,700 |

Zealow Ltd – Statement of Financial Position as at 31 December 2015

| GH¢’000 | GH¢’000 | GH¢’000 |

|---|---|---|

| Non-current assets | ||

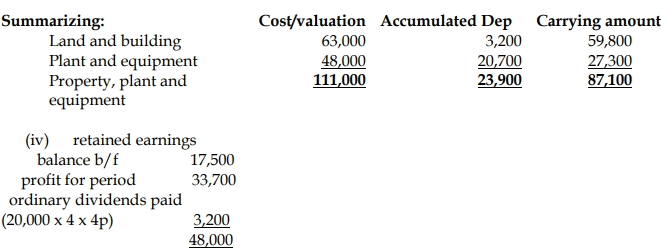

| Property, plant and equipment (w(iv)) | 87,100 | |

| Investment property (w(ii)) | 13,500 | |

| Total non-current assets | 100,600 | |

| Current assets | ||

| Inventories (10,500 – 300 (w(i))) | 10,200 | |

| Trade receivables (13,500 + 1,500 JV) | 15,000 | |

| Total current assets | 25,200 | |

| Total assets | 125,800 | |

| Equity and liabilities | ||

| Ordinary shares of 25p each | 20,000 | |

| Reserves: | ||

| Revaluation | 21,000 | |

| Retained earnings (w(v)) | 48,000 | |

| Total equity | 89,000 | |

| Non-current liabilities | ||

| Deferred tax (w(iii)) | 3,600 | |

| Redeemable preference shares of GH¢1 each | 10,000 | |

| Total non-current liabilities | 13,600 | |

| Current liabilities | ||

| Trade payables (11,800 + 2,500 JV) | 14,300 | |

| Bank overdraft | 900 | |

| Current tax payable | 8,000 | |

| Total current liabilities | 23,200 | |

| Total equity and liabilities | 125,800 |

The damaged inventories will require expenditure of GHC450,000 to repair them then

have an expected selling price of GHC950,000. This gives a net realizable value of

GHC500,000, as their cost was GHC500,000, as their cost was GHC800,000, a write

down of GHC300,000 is required.

(i) The fair value model in IAS 40 investment property requires investment

properties to be included in the balance sheet at their fair value (in this case

taken to be the open market value). Any surplus or deficit is recorded in

income

(ii)

Taxable temporary differences are GHC12 million. At a rate of 30% this would require a

balance sheet provision for deferred tax of GHC3.6 million. The opening provision is

GHC5.2 million, thus a credit of GHC1.6 million, thus a credit of GHC1.6 million will be

made in the statement of profit or loss.

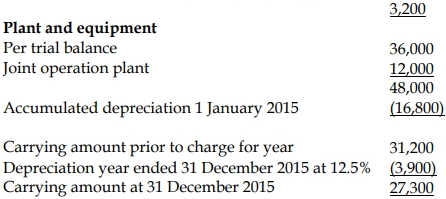

(iii) Non-current assets

Land and building

Depreciation of the building for the year ended

31 December 2015 will be (48,000/15 years)