Question

Answer

Memorandum

To: The Board of Directors

From: The Finance Manager

Date: 3rd April 2022

Subject: Analysis of the performance of Boomu Ltd

The performance of Boomu Ltd for the year ended 31 December 2021 has been assessed in this report. The performance of Sintim Ltd, a competitor, is used as a benchmark. The ratios used include profitability, working capital management, and gearing.

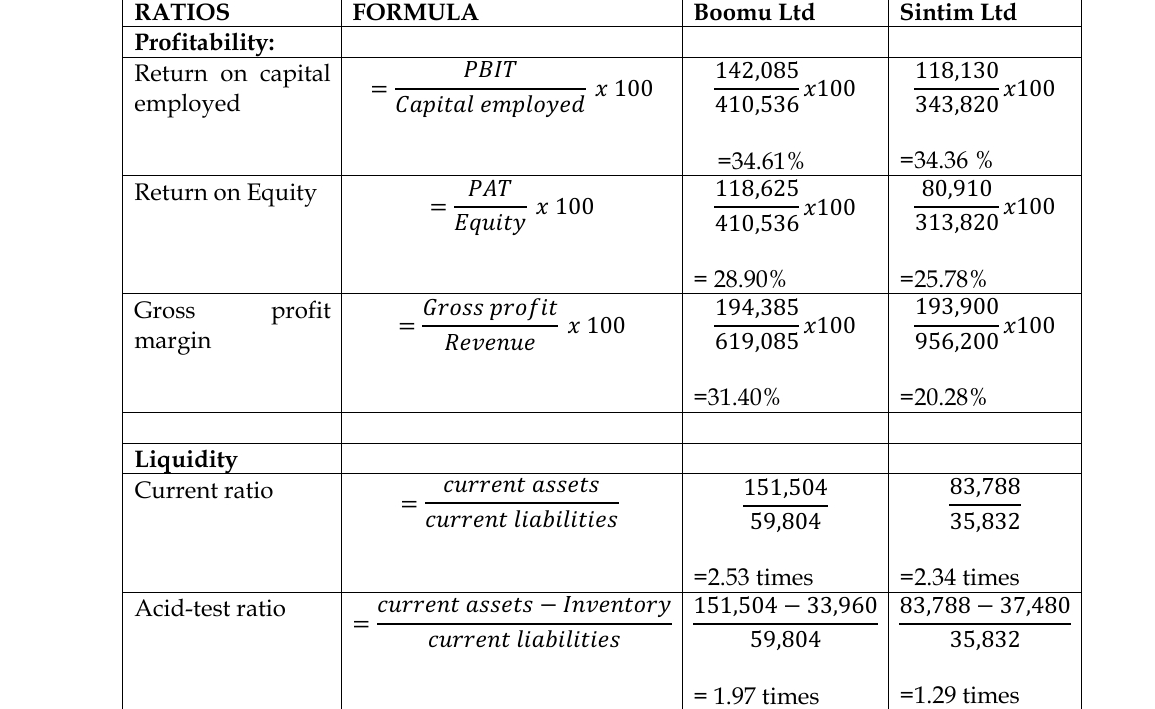

Profitability:

- The revenue of Boomu Ltd was 35.26% lower than that of Sintim Ltd. However, Boomu Ltd generated higher returns for all investors.

- Boomu Ltd’s return on capital employed was 34.61%, while Sintim Ltd had a return of 34.36%.

- Boomu Ltd also generated a higher return on equity (28.90%) compared to Sintim Ltd (25.78%).

- The gross profit margin was higher for Boomu Ltd (31.40%) than Sintim Ltd (20.28%), indicating better control over cost of sales.

Liquidity:

- Boomu Ltd’s current ratio was 2.53 times compared to 2.34 times for Sintim Ltd, suggesting better liquidity.

- The acid-test ratio of Boomu Ltd was 1.97 times, higher than Sintim Ltd’s 1.29 times, indicating that Boomu Ltd had more current assets (excluding inventory) to cover liabilities.

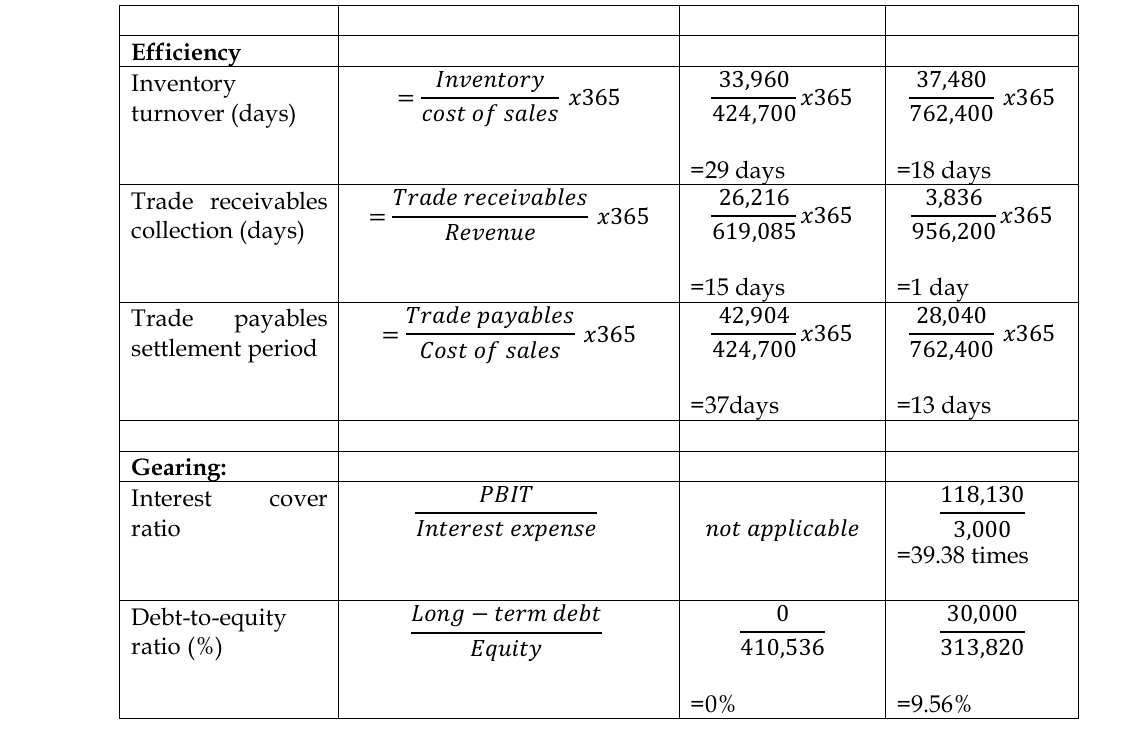

Efficiency:

- Boomu Ltd’s inventory turnover was 29 days, higher than Sintim Ltd’s 18 days, indicating that Sintim Ltd was faster at selling its inventory.

- Boomu Ltd took 15 days to collect receivables, whereas Sintim Ltd took just 1 day, showing superior efficiency in receivables management for Sintim Ltd.

- Boomu Ltd had a trade payables settlement period of 37 days, compared to Sintim Ltd’s 13 days, indicating that Boomu Ltd had better credit terms from suppliers.

Gearing:

- Boomu Ltd is fully equity-financed, meaning no financial risk to shareholders from debt. Sintim Ltd, however, had debt in its capital structure, with a debt-to-equity ratio of 9.56%.

Conclusion: Boomu Ltd performed better than Sintim Ltd in terms of profitability and liquidity but lagged in inventory and receivables management.

Appendix:

(1/4 mark for each correct computation of ratio = 5 marks; 15 marks for the report)

(1/4 mark for each correct computation of ratio = 5 marks; 15 marks for the report)

(Total = 20 marks)