Question

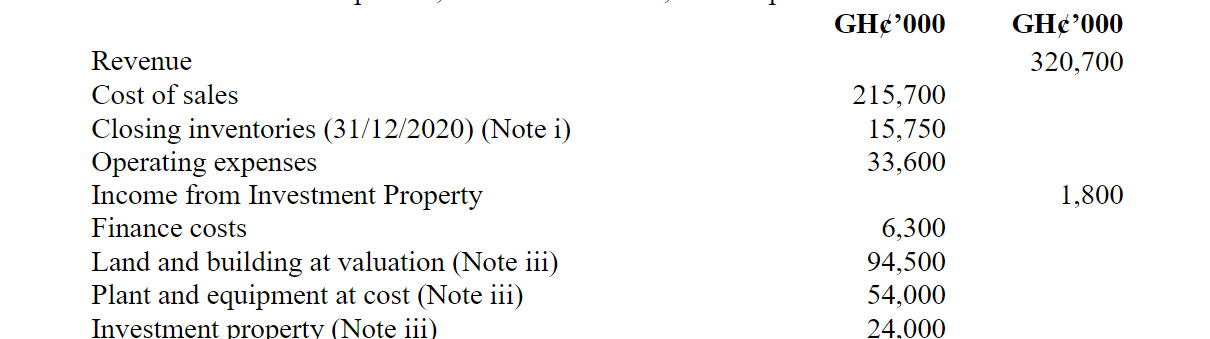

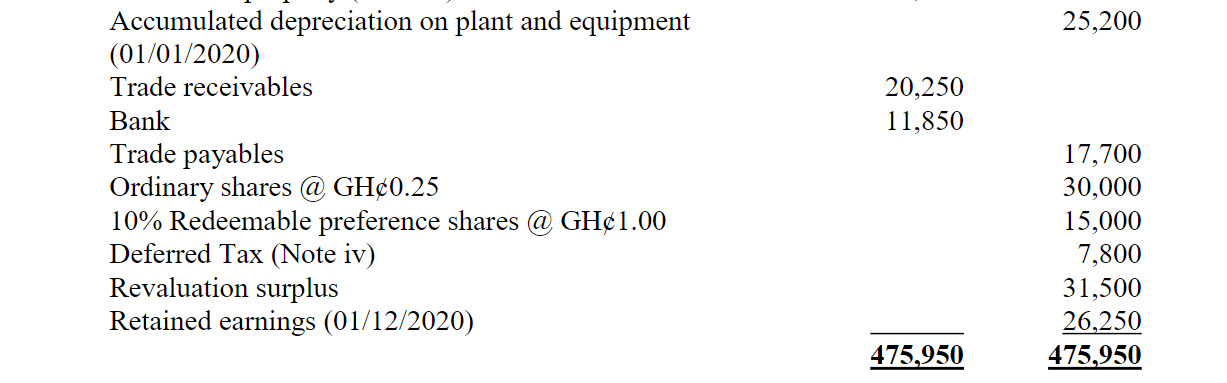

The trial balance of Caput Plc, as at 31 December, 2020 is provided below:

Additional Information:

1. An inventory count at 31 December 2020 amounted to GH¢15,750,000. This includes damaged goods with a cost of GH¢1,200,000. These will require remedial work costing GH¢675,000 and could be sold for GH¢1,425,000.

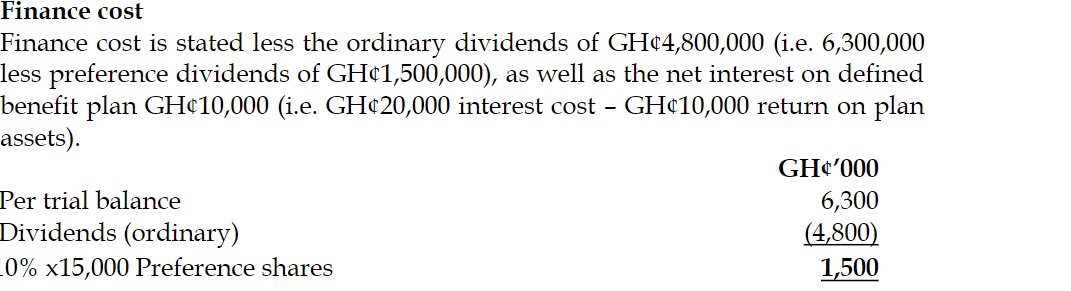

2. Finance cost is made up of the full year’s preference and ordinary dividends paid.

3. Non-Current Assets:

- Land and Building were revalued at GH¢22,500,000 and GH¢72,000,000 respectively on 1 January 2020, resulting in revaluation gain of GH¢11,000,000 for the current year. At that date, the remaining life of the building was 15 years. Depreciation is on a s

- Depreciation on Plant and Equipment is at 12.5% on a reducing balance basis.

- Investment Property: On 31 December 2020, a qualified surveyor valued the property at GH¢20,250,000. Caput Plc uses the fair value model under IAS 40: Investment Property to value its investment property.

- It is the policy of the company to charge depreciation on a full-year basis

traight-line basis. Ignore deferred tax implications.

.

4. The directors have estimated the provision for income tax for the year ended 31 December 2020 at GH¢12,000,000. The deferred tax for the year ended 31 December 2020 is to be adjusted so that the tax base of the company’s net assets is GH¢18,000,000 less than the carrying amount. Assume the rate of tax is 30%.

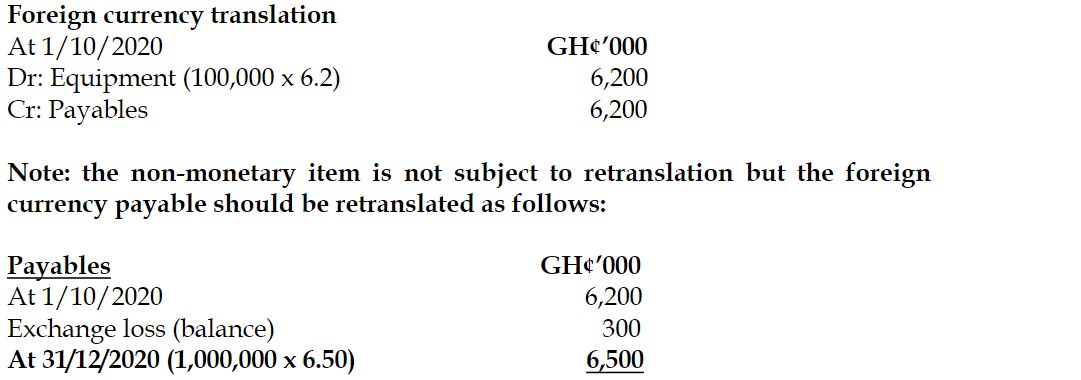

5. On 1 October 2020, Caput Plc imported a piece of equipment from a European supplier for €1 million and agreed to settle the bill in six months’ time. The relevant exchange rates are provided below:

No entries have been made for the above transaction. Any exchange difference on translation should be debited or credited to operating expenses.

Required:

Prepare for Caput Plc:

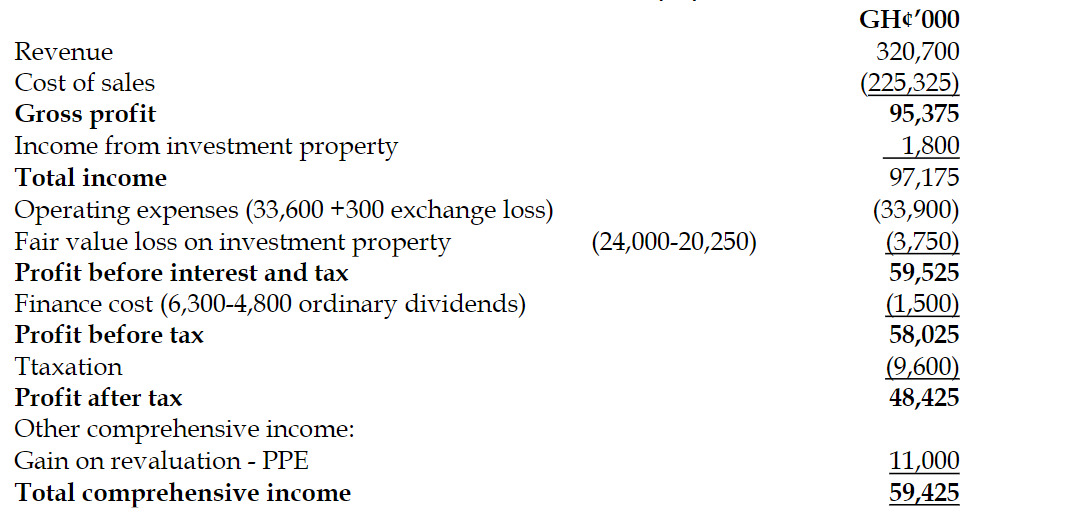

a) Statement of Comprehensive Income for the year ended 31 December 2020. (10 marks)

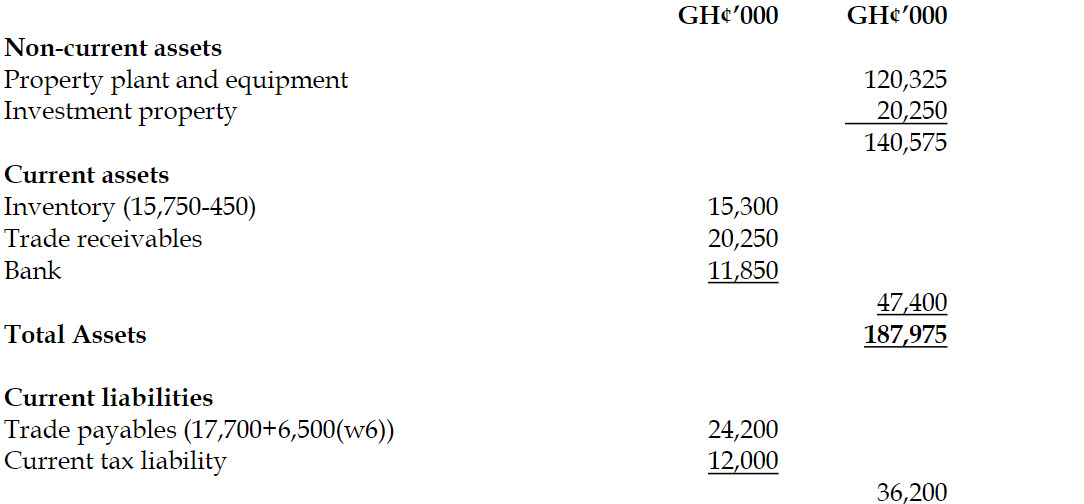

b) Statement of Financial Position as at 31 December 2020. (10 marks)

Answer

a)

CAPUT LIMITED

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE

INCOME FOR THE YEAR ENDED 31/12/2020

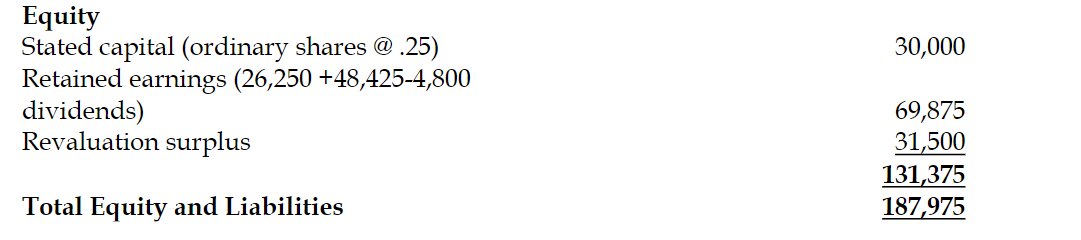

b)

CAPUT LIMITED

STATEMENT OF FINANCIAL POSITION AS AT 31/12/2020

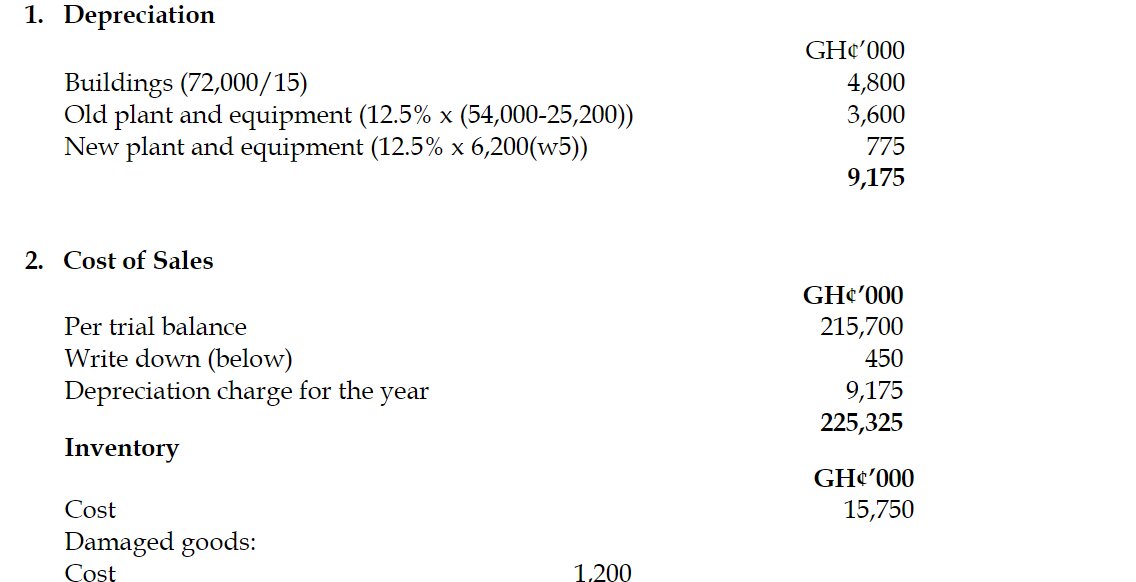

WORKINGS: 1. Depreciation

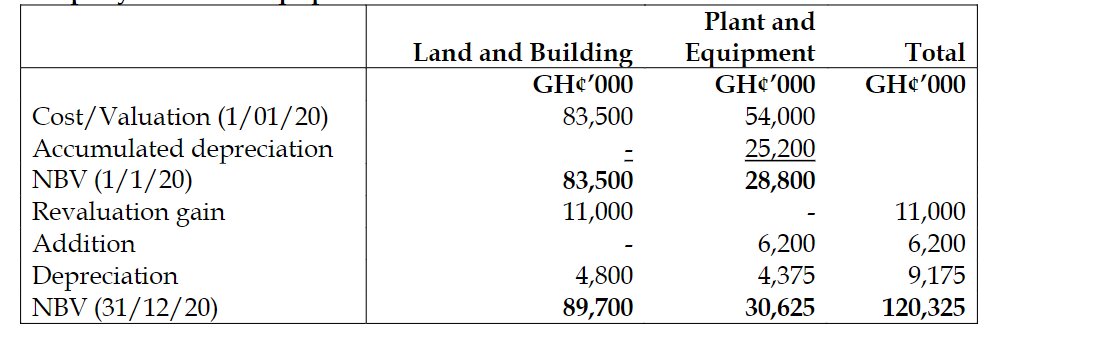

3. Property Plant and Equipment

Depreciation charge on building per annum = 72 m/15 years = 4.8m

Depreciation charge on Plant and Machinery is 12.5% x (54 m-25.2 m) = 3.6m

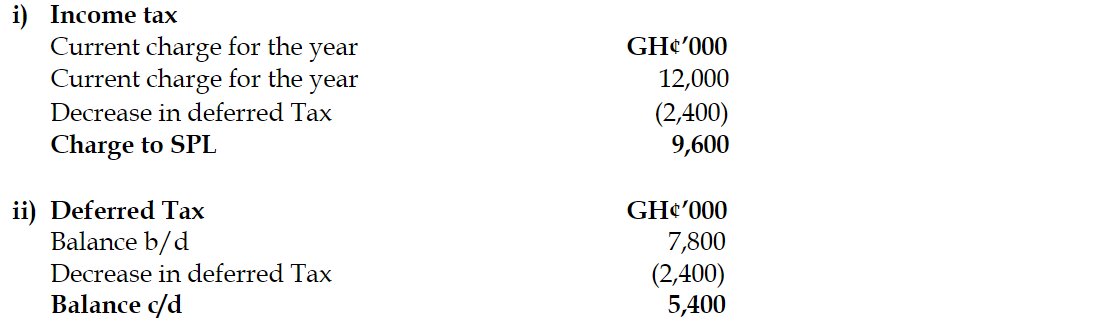

4. Taxation

NB: Deferred tax liability at year end = 30% x 18,000,000 (temporary timing difference) = GH¢5,400,000.

5.

6.

80 ticks @ 0.25