Question

Answer

a) i) Value based on P/E ratio of Blanco

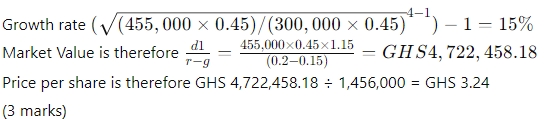

Market Value = P/E ratio x Earnings = 8 × 455,000 = GHS 3,640,000.00

Price per share is therefore GHS 3,640,000.00 ÷ 1,456,000 = GHS 2.50

(3 marks)

ii) Gordon’s growth model

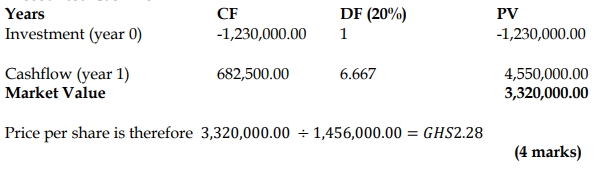

iii) Discounted Cash flow

b) Problems with the various valuation methods

- P/E ratio:

- The use of another company’s P/E ratio suggests that the two companies have similar characteristics. If Zinko management is not satisfied with the price, they can raise objections.

- The P/E ratio does not take into account the growth prospects of the company. The use of past earnings can be objected to by the management.

- The method is not scientific and hence subjective.

- Dividend growth model:

- The estimation of growth is based on past records, suggesting that the future of the company will be the same as its past, which may be inaccurate.

- The discount factor (expected returns) must be greater than the growth rate for the model to work; otherwise, the results would be negative or zero.

- Non-dividend-related factors are not taken into consideration. This means a company trying to generate internal cash flow to undertake a project that would generate substantial earnings would have a lower value if dividends are not paid.

- Discounted cashflow model:

- Management can raise concerns about how the future cash flows were estimated.

- The growth rate estimate and the fact that it remains constant into perpetuity raises concerns about the objectivity of the method.

- The use of a new cost of capital can be challenged since it may not reflect the risk profile of the operations of Zinko.

- The method is not scientific and hence subjective.

(6 marks)

c) Reasons for the acquisition of another company

- Growth from this transaction is much faster than internally developed growth.

- The companies would have access to new products, markets, and customers, which would have been difficult to achieve by a single company.

- Acquisitions enable companies to break through into other parts of the industry even when there were entry restrictions.

- Acquisitions help to take advantage of the competition, especially where keen competitors had plans of acquiring the target for competitive purposes.

- Acquisitions lead to economies of scale, which means cost savings, higher profits, and higher market value.

- Acquisitions help to access some technical expertise and technologies that may not be readily available on the market.

(4 points @ 0.5 marks = 2 marks)