Question

Answer

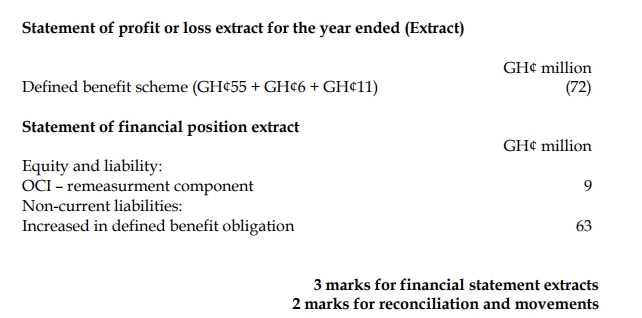

The defined benefit scheme for the year should have been recorded as follows:

| Description | GH¢’million |

|---|---|

| Net obligation at 31 December 2019 | 120 |

| Cash contribution into the scheme | (100) |

| Net finance cost for the year (GH¢120 million x 5%) | 6 |

| Current service cost | 55 |

| Loss on curtailment | 11 |

| Gain on remeasurement | (9) |

| Net liability at 31 December 2020 | 83 |

The benefits paid do not affect the net liability for the year. Since only the cash contributions have been recorded for the year, the net obligation should be increased by GH¢63 million (GH¢83 million – GH¢20 million). GH¢72 million should be expensed to profit or loss, being the service cost component (current and curtailment) plus the interest charge. GH¢9 million should be credited to other components of equity, being the gain on remeasurement.