Question

Answer

a) Jeanne Cosmetics Ltd:

i) With a maturity value of GH¢105,000 received for investing a principal of GH¢100,000, the company earned GH¢5,000 in interest over the 3-month investment period. Thus, the implied interest rate for the investment period is 5%:

Holding Period Interest=![]()

Holding Period Interest=![]()

(2 marks)

ii) If only the principal is rolled over while the interest rate remains the same, the company will receive a cedi return of GH¢5,000 on the principal of GH¢100,000 at the end of each of the four investment periods (i.e., 3 months) in a year. The annual simple interest rate will be 20%:

Annual Simple Interest=![]()

Annual Simple Interest=![]()

Alternatively, the annual simple interest may be calculated as the product of the holding period interest rate and the number of times it will be earned in a year:

Annual Simple Interest![]()

iii) If both the principal and interests are rolled over while the interest rate remains the same, the initial principal will effectively be compounded by a periodic interest factor of 1.05 (i.e., 1 + 5%) every 3 months for a year. The annual compound interest rate will be 21.55%:

Alternatively, the annual compound interest may be calculated as the effective annual rate:

Annual Compound Interest=![]()

Annual Compound Interest=![]()

b) Apphia Fabrics Ltd:

Sinking fund

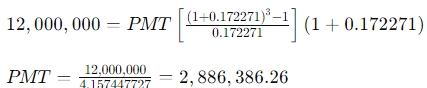

As the objective of the fund is to raise enough money to finance the acquisition of a newer version of its plant in three years’ time, the future value of the fund (F) should be equal to the forecasted cost of the newer version of the plant in three years’ time (Cost):

![]()

As the deposits are to be made at the beginning of each period, the case is that of an annuity due. And as the future value is known, the annual deposit can be calculated using the future value formula of an annuity due:

![]()

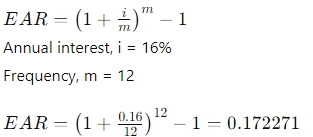

As there are annual deposits and multiple compounding in each year, the appropriate interest rate to use is the effective annual rate, and the period should be in years.

The effective annual interest rate is 17.2271%:

The amount of each annual deposit is GH¢2,886,386.26:

![]()

The future value of the fund, F_3 = GH¢12,000,000

Annual interest, i = 17.2271%

Number of periods, n = 3 years

c) Aduro Pharmaceuticals Plc:

i) Identification of the type of currency risk exposure the company is facing

- Case 1: Transaction exposure to currency risk

- Case 2: Translation exposure to currency risk

(1 mark for each case = 2 marks)

ii) Internal strategies for dealing with currency risk exposure

Case 1 is a transaction exposure to currency risk involving a pound sterling payable that is subject to the adverse effect of a probable depreciation in the local currency relative to the foreign currency in which it is denominated. The Treasury Department of the company may use any of the following internal strategies to deal with the currency risk exposure:

- Invoice currency: A way of avoiding the currency risk exposure altogether is to invoice or be invoiced in the entity’s local currency. This strategy effectively shifts the currency risk exposure to the counterparty. The Treasury Manager of Aduro Pharmaceuticals may renegotiate with the lender for the company to be allowed to settle the obligations related to the loan in its local currency.

- Leading and lagging: To avoid a potential currency loss in the future, an entity may collect the underlying foreign currency receivable or pay the underlying foreign currency payable earlier (i.e., leading). And to enjoy a potential currency gain in the future, an entity may delay the collection of the underlying foreign currency receivable or the payment of the underlying foreign currency payable (i.e., lagging). In the case under review, the underlying exposure is a payable and the local currency is expected to depreciate against the foreign currency. That suggests a potential currency exchange loss. Thus, the Treasury Department may consider leading the settlement of the loan to avoid the potential currency exchange loss.

- Matching: To reduce an entity’s underlying exposure in a currency, its receivables and payables in that currency may be set off to a lower net receivable or payable. If the company has some receivables in the pound sterling, the Treasury Department should consider matching them. Otherwise, the company may consider exporting some of its output for the foreign currency to match the resulting receivables against the payables under the loan contract.

External strategies for dealing with currency risk exposure:

- Forward hedge: A forward hedge involves the use of forward contracts to lock the exchange rate at a certain rate to secure the outcome of the underlying exposure. The company may enter a forward contract to buy pound sterling forward at an agreed rate. That would effectively convert the underlying exposure, the outcome of which is uncertain due to potential changes in the exchange rate, to a certain outcome as the exchange rate is locked at the forward exchange rate.

- Money market hedge: A money market hedge involves entering a couple of money market transactions (i.e., borrowing and investing) that effectively converts a foreign currency receivable or payable to a guaranteed local currency receivable or payable. To hedge the underlying pound sterling payable, the Treasury Department would borrow the local currency, buy pound sterling with that, and invest the pound sterling. The maturity value of the pound sterling investment will then be used to offset the pound sterling payable, leaving the maturity value of the local currency borrowing as the guaranteed outcome.

- Futures hedge: A futures hedge involves buying or selling a futures contract for potential payoffs to offset actual losses from the underlying exposure. To hedge the underlying pound sterling payable, the Treasury Department would buy pound sterling futures now for settlement in the future. When the underlying exposure falls due, the Treasury department would then close the company’s position by selling futures. Any gains from futures can be used to offset potential losses from the actual settlement of the underlying exposure.

- Option hedge: An option hedge involves buying an option for the right to buy or sell the underlying asset at a given price. This provides the company with the opportunity to benefit from gains from the option to offset losses from the underlying exposure while avoiding downside risk. A non-refundable premium is paid for the right to buy or sell. To hedge the underlying exposure with an option, The Treasury Department would buy a call option on the pound sterling, so the company gets the right to buy pounds at the agreed strike price.

- Currency swap: Hedging with a currency swap involves entering a swap arrangement with a counterparty to exchange periodic payments in different currencies over a period. A currency swap permits an entity to make payments in its preferred currency. To hedge with a currency swap, the Treasury Department would arrange with a swap counterparty to undertake to swap interest and principal payments in the local currency and pound sterling. Under that arrangement, the company would get to pay interest in cedis and repay the principal in cedis.