Question

Answer

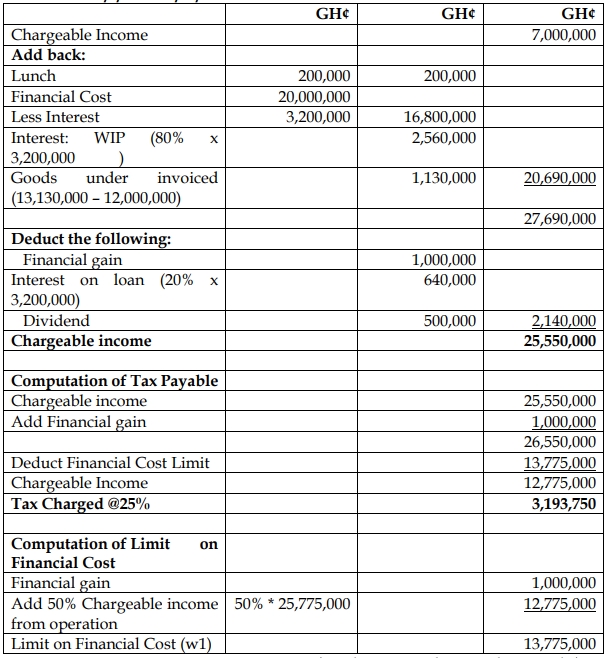

i) Computation of Tax Payable:

ii) Tax Implications of Staff Lunch, Interest Paid, and Dividend Received:

- Staff Lunch (GH¢200,000):

- If the benefit provided by the lunch cannot be allocated to specific staff members, it is considered a non-deductible expense for corporate tax purposes.

- The expense is personal in nature, not related to business operations, and should be disallowed for tax purposes.

- Interest Paid on Loans (GH¢3,200,000):

- Interest related to capital work in progress (80% of the total interest, GH¢2,560,000) must be capitalized and cannot be deducted in the current year.

- Interest related to working capital (20%, GH¢640,000) is an allowable expense and can be deducted for tax purposes.

- Dividend Received (GH¢500,000):

- Dividends from a resident company where the recipient holds less than 25% voting power are subject to an 8% withholding tax. In this case, GH¢500,000 is taxable at 8%.

iii) Tax Planning Measures to Reduce Tax Liability Related to Dividend:

- Increase Ownership in Ann Ltd:

Under Section 59 of the Income Tax Act, 2015 (Act 896), dividends from a resident company where the recipient holds at least 25% of the voting power are exempt from tax. Conti Ltd currently holds 24% in Ann Ltd, so increasing its ownership to 25% or more would make the dividend income exempt from tax.

iv) Tax Implication of Financial Cost from Derivative Transactions:

- Financial costs from derivative transactions (GH¢20,000,000) are only deductible up to the sum of the financial gain from derivatives (GH¢1,000,000) and 50% of the chargeable income before adjusting for the financial cost.

- Any financial cost exceeding this limit is not deductible in the current year and can be carried forward for the next five years.

- Impact: The disallowed portion of the financial cost erodes the company’s profitability and increases its tax liability, as it cannot be deducted in the current year.