Question

Answer

a) Capital Structure Decision at Moore Plastics Ltd

i) Reasons for Following the Pecking Order

- Easier Access to Funds: Managers prefer sources of finance that are easier to access. Retained earnings, being the easiest to access and use, are the first choice. Borrowing comes next, as it is often easier to obtain compared to issuing new equity, which is typically the last resort due to its higher complexity and cost.

- Lower Issue Costs: Managers prefer financing sources with lower issue costs. Retained earnings have no issue costs, making them highly preferred. Debt usually has lower issuance costs compared to equity, thus it is favored over new equity offers.

- Signaling Effect: Managers believe that debt issuance sends a positive signal to the market about the company’s future prospects, indicating that management is confident about generating sufficient profits to cover the debt. Conversely, issuing new equity may be interpreted as a lack of confidence, leading to a decline in share price.

- Investors’ preference for safer securities: As debt stocks offer more secured

income streams to investors than equity stocks offer, it is easier for firms to

raise funds through debt offers than equity offers.

ii) Factors to Consider When Redesigning Capital Structure

- Business Risk: Business risk refers to the risk inherent in the company’s operations without considering debt. If Moore Plastics Ltd faces high business risk, the new capital structure should have a higher proportion of equity to reduce the risk of financial distress. If business risk is low, the company can afford to have a higher proportion of debt.

- Financial Risk: Financial risk is the additional risk to shareholders due to the use of debt. If the company already has high financial risk (i.e., high levels of debt), then the new capital structure should emphasize more equity to avoid excessive leverage. Conversely, if financial risk is low, the company might consider increasing its debt level.

- Tax position: The tax-benefit from the use of debt financing is high when the

company falls into a higher tax bracket. If the company is in a higher tax

bracket, a financing structure with more debt than equity would be

reasonable. - Clientele effect: An investor would prefer a particular capital structure to

another. So when redesigning capital structure, directors should consider

how present and prospective investors will react to the new capital structure.

b) Appropriate Cost of Capital for Pusher Mining Ltd’s New Oil Project

Calculation of WACC for the New Project

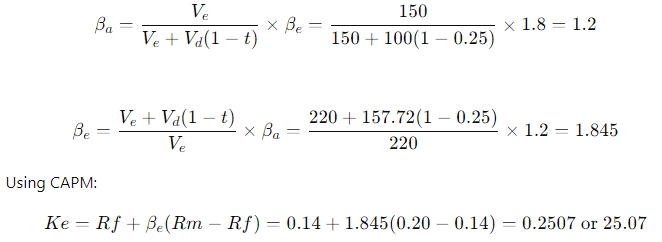

- Cost of Equity (Ke):

To calculate the cost of equity, we use the Capital Asset Pricing Model (CAPM).

- Equity Beta of Cargo Oil Ltd: 1.80

- Ungeared (Asset) Beta of Cargo Oil Ltd: 1.2

- Market value of Cargo Oil Ltd’s equity: GH¢150 million

- Market value of Cargo Oil Ltd’s debt: GH¢100 million

- Regear to reflect Pusher Mining Ltd’s capital structure:

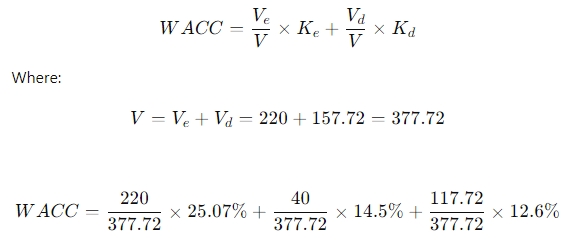

- Cost of Debt (Kd):

- After-tax cost of bank loans: 14.5%

- After-tax cost of bonds:Bondholders will prefer to convert their bonds into shares because the conversion value (GHS118.7) is higher than the redemption value (GHS100).Cost of bonds (IRR)=12.6

- WACC Calculation:

- Market value of equity (Ve): GHS220 million (40 million shares × GHS5.5/share)

- Market value of debt (Vd): GHS157.72 million (GHS40m bank loans + GHS117.72m bonds)

Conclusion:

The appropriate cost of capital Pusher Mining Ltd should use to appraise the new oil project is 20.1%. This WACC reflects both the business risk associated with the oil industry and the financial risk of the company’s capital structure.