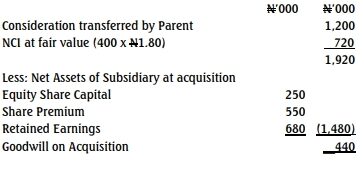

A parent acquired 600,000 equity shares of its subsidiary three years ago for N1,200,000. The subsidiary’s issued equity share capital on that date was N250,000, with each share having a nominal value of 25 kobo. Other components of the subsidiary’s net assets at the acquisition date included share premium of N550,000 and retained earnings of N680,000. The subsidiary’s shares were quoted at N1.80 per share when the parent took control.

Required: Calculate the goodwill on acquisition if the parent measures non-controlling interest at its fair value.