Question

Answer

To: MD of ANN Co

From: Accountant

Date: XX.XX.XX

Subject: The Financial Position of IB Co Ltd

Introduction:

This report has been prepared on the basis of the three most recent financial statements of IB Co Ltd, covering the years 2013 to 2015 inclusive. The financial analysis focuses on two key areas: gearing and liquidity ratios.

Debt and Gearing:

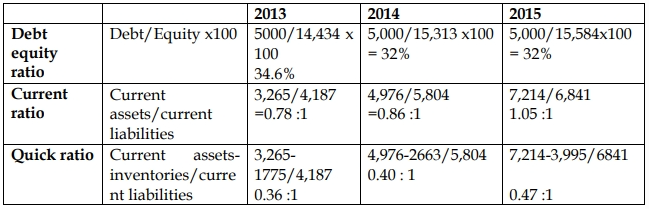

- The gearing ratio (debt to equity) measures the proportion of a company’s interest-bearing debt finance relative to its equity finance (shareholders’ funds).

- For IB Co Ltd, the gearing ratio is calculated as follows:

- 2013: (5,000 / 14,434) x 100 = 34.6%

- 2014: (5,000 / 15,313) x 100 = 32%

- 2015: (5,000 / 15,584) x 100 = 32%

Although we do not have the industry norm for comparison, IB Co Ltd’s gearing ratio appears reasonable. However, it is notable that the ratio has remained relatively stable over the three years, indicating no significant reduction in debt levels. The company continues to rely heavily on debt finance, which may expose it to financial risk, especially with rising interest rates or reduced profitability.

Liquidity Ratios:

- The current ratio measures a company’s ability to meet its current liabilities out of current assets. It is calculated as follows:

- 2013: 3,265 / 4,187 = 0.78:1

- 2014: 4,976 / 5,804 = 0.86:1

- 2015: 7,214 / 6,841 = 1.05:1

Although the current ratio has improved over the period, IB Co Ltd’s ability to meet its short-term liabilities was inadequate in 2013 and 2014. A ratio of at least 1:1 is generally expected, and while IB Co reached this benchmark in 2015, the prior years were concerning.

- The quick ratio (acid-test ratio) excludes inventories from current assets to assess the company’s ability to meet short-term liabilities using its most liquid assets:

- 2013: (3,265 – 1,775) / 4,187 = 0.36:1

- 2014: (4,976 – 2,663) / 5,804 = 0.40:1

- 2015: (7,214 – 3,995) / 6,841 = 0.47:1

The quick ratio is particularly concerning as it shows that IB Co Ltd would not be able to meet its current liabilities without relying on the sale of inventory. This is a liquidity risk, and the company’s reliance on inventory to cover short-term obligations should be closely monitored.

Conclusion:

IB Co Ltd’s financial position shows some improvements, particularly in the current ratio, but there are concerns about its liquidity as indicated by the quick ratio. It is recommended that further investigation is carried out to understand:

- The nature of the company’s bank facilities and its reliance on short-term financing.

- The inventory turnover period and whether the company’s reliance on inventories for liquidity is sustainable.

- The terms of its debt, particularly the 12% debentures, and whether refinancing might be a possibility to reduce interest expenses.

Additionally, comparing IB Co Ltd’s ratios with industry averages would provide a better perspective on its financial health.

Workings – Calculation of Relevant Ratios: