Question

Answer

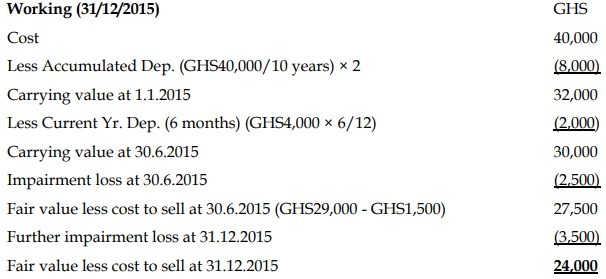

Under IFRS 5 Non-current Assets Held for Sale and Discontinued Operations, non-current assets classified as held for sale should be measured at the lower of carrying amount and fair value less costs to sell. The following steps outline how the plant should be accounted for:

Conclusion:

-

- The plant should be recognised as an asset held for sale at GH¢24,000 in the statement of financial position as of 31 December 2015.

- A total impairment loss of GH¢6,000 (GH¢2,500 + GH¢3,500) should be recognised in the statement of profit or loss for the year.