Question

Answer

| Description | Amount (GH¢) | Rate | Withholding Tax (GH¢) |

|---|---|---|---|

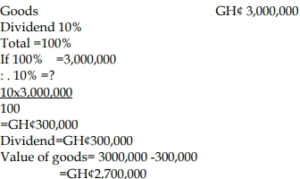

| Goods (Net of Dividend) | 2,700,000 | 3% | 81,000 |

| Dividend | 300,000 | 8% | 24,000 |

| Consultancy Services (50%) | 600,000 | 7.5% | 45,000 |

| Management & Technical Services | 600,000 | 7.5% | 45,000 |

| Total Withholding Tax Payable | 255,000 |

Reasons for Withholding Tax Imposition:

- To ensure early collection of taxes at the source of payment.

- To enhance tax compliance and reduce tax evasion by collecting taxes upfront.