Question

Answer

i) Flexible Budget:

A flexible budget is a budget that recognizes differences between fixed and variable costs when the volume of activity changes. Flexible budgets are useful for control purposes as the actual volume of activity may be compared to the budget by flexing the budget so that it is based on actual activity. Flexible budgets cannot be prepared until the end of a budget period.

(2 marks)

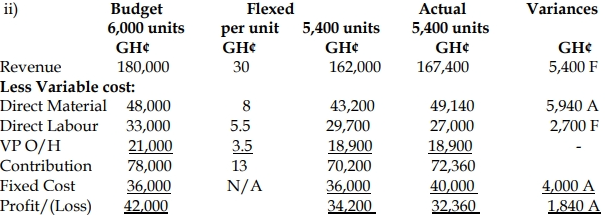

ii) Flexible Budgeted Operating Statement:

(7 marks evenly spread using ticks)

iii) Reasons Why the Original Operating Statement Was of Little Use to Management:

- A static budget is fixed for the entire period covered by the budget, with no changes based on actual activity. Thus, even if actual sales volume changes significantly from the expectations documented in the static budget, the amounts listed in the budget are not changed.

- In more dynamic environments where operating results could change substantially, a static budget can be a hindrance, since actual results may be compared to a budget that is no longer relevant.

(2 marks)

iv) Non-Financial Measures Otuo Could Use to Monitor Performance:

- Speed of food delivery. Customers at fast food restaurants expect their food order to be served quickly. If Otuo is to be successful, it must achieve fast food delivery. Therefore, a measure of time from customer order to food service is a key metric to monitor in ascertaining the restaurant’s success at this requirement.

- Number of repeat customers. Otuo operates in a small town that offers a number of other choices of fast food restaurant to its residents. If Otuo is to establish itself and grow market share, the restaurant needs to develop a loyal customer base. Number of repeat customers is a measure that could indicate the sustainability of the business and future financial success.

- Cleanliness of the environment

- Courtesy of waiters and waitresses

- Responsiveness of service

- Availability of food