Question

Answer

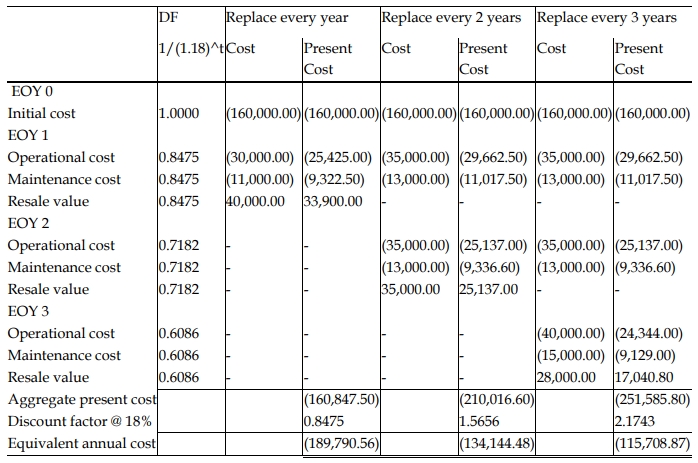

Calculation of the Equivalent Annual Cost (EAC) for different replacement cycles:

1-year Cycle: If the plant is replaced every year, the firm will incur the initial cost of GH¢160,000 now, operational cost of GH¢30,000 at the end of year one, maintenance cost of GH¢11,000 at the end of year one, and receive the resale value

of GH¢40,000 at the end of year one when the asset is replaced.

2-year Cycle: If the plant is replaced every two years, the firm will incur the initial cost of GH¢160,000 now; operational cost of GH¢30,000 and GH¢35,000 at the end of year one and year two respectively; maintenance cost of GH¢11,000 and GH¢13,000 at the end of year one and year two respectively; and receive the resale value of GH¢35,000 at the end of year two when the plant is replaced.

3-year Cycle: If the plant is replaced every three years, the firm will incur the initial cost of GH¢160,000 now; operational cost of GH¢30,000, GH¢35,000 and GH¢40,000 at the end of year one, year two and year three respectively; maintenance cost of GH¢11,000, GH¢13,000 and GH¢15,000 at the end of year one and year two respectively; and receive the resale value of GH¢28,000 at the end of year two when the plant is replaced.

Calculation of the Equivalent Annual Cost (EAC):

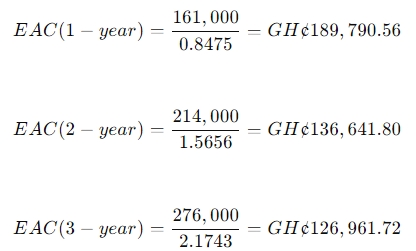

The equivalent annual cost (EAC) for each cycle can be calculated using the formula:

Using the cost of capital (18%):

- 1-year cycle PVIFA = 0.8475

- 2-year cycle PVIFA = 1.5656

- 3-year cycle PVIFA = 2.1743

Conclusion:

The optimal replacement cycle is the 3-year cycle because it results in the lowest equivalent annual cost of GH¢126,961.72.

(Marks allocation: 1 mark for cash flows of each of the three cycles = 3 marks; 1 mark for PVIFA for each of the three cycles = 3 marks; 0.5 marks for the equivalent annual cost for each of the three cycles = 1.5 marks; optimal replacement cycle = 1 mark = total: 10 marks)