Question

Answer

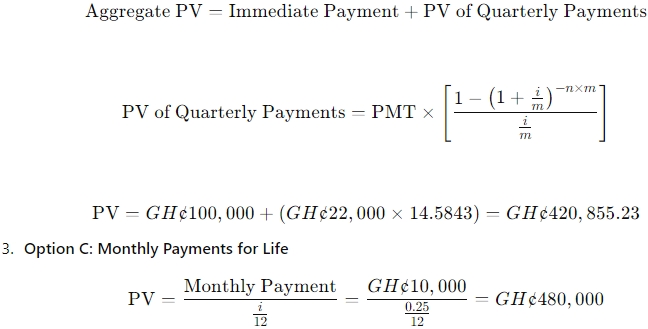

a) Best Pay-out Option for Mr. Akolgo:

- Option A: Lump Sum Payment

Since it is a lump sum to be paid now, it is already in its present value (PV), which is GH¢400,000. - Option B: Quarterly Payments

The present value is the sum of the immediate payment and the present value of the quarterly payments.

Recommendation: Option C is recommended as it provides the highest present value.

(Marks allocation: Computation for Option B = 3 marks; Computation for Option C = 2 marks; Recommendation = 1 mark)

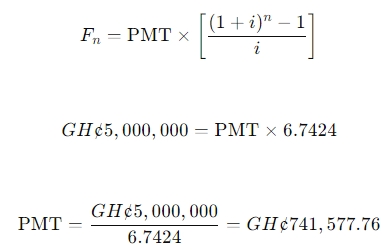

b) Annual Deposit for Sinking Fund:

The future value of the fund (F) should be equal to the principal to be repaid in five years’ time:

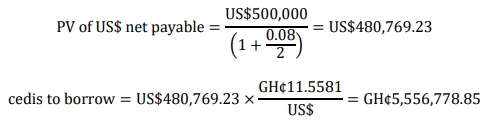

c) Money Market Hedge Setup and Outcome:

i) Setup:

- The underlying exposure is a US$500,000 net payable (payment minus receipt), which is a liability.

- Position in International Money Market: Invest US$ at the investing rate of 8%.

- Position in Domestic Money Market: Borrow cedis at the cedi borrowing rate of 25%.

(3 marks)

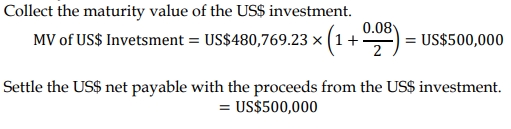

ii) Evaluation of the Outcome:

- Borrow cedi equivalent of the present value of the US$ net payable:

**The offer rate is used as dollars will be bought with the cedis borrowed. - Invest the US$480,769.23 bought at the US$ investing rate

- Settle the US$ net payable with the proceeds from the US$ investment:

Net Outcome: The money market hedge results in a net cost of GH¢6,251,376.21