Question

Answer

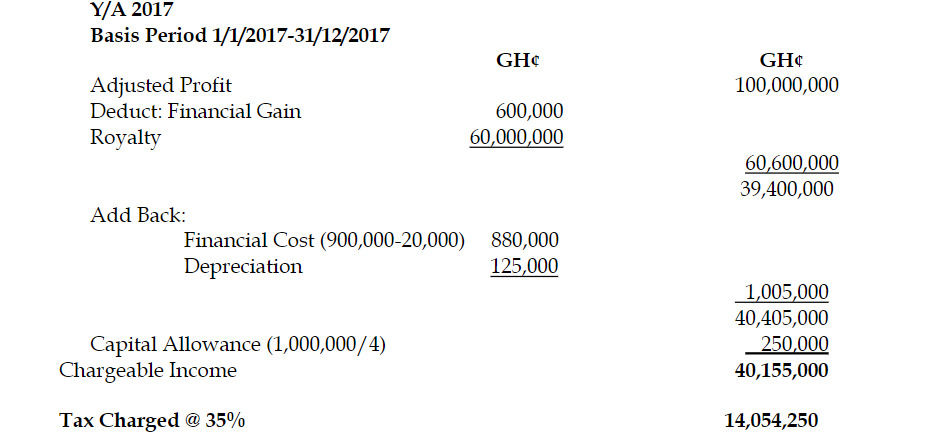

i) Kaato Mining Company Ltd

Computation of Tax Payable

(6 marks evenly spread using ticks)

ii) Treatment of Financial Cost: Under mining, any financial cost shall be used against financial gain. Any financial cost remaining shall be carried forward for the next five (5) years. If there is no financial gain, the financial cost shall be carried forward

(2 marks)