Question

Answer

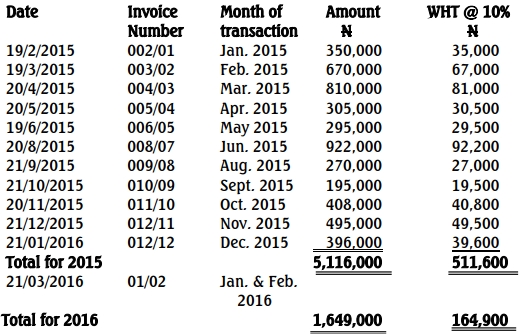

(a) Oloriogun Logistics Limited

Calculation of Withholding Tax Credits Based on the Invoices:

(a) Calculation of Withholding Tax Credits Based on the Invoices:

(b) Total Amount of Withholding Tax Credits to be Claimed for Each Year of Assessment (Assuming no other transactions after February 2016):

- 2016 Year of Assessment: N511,600

- 2017 Year of Assessment: N164,900

(c) Due Date for Remitting Withholding Tax Returns:

- Withholding tax returns should be remitted to the relevant tax authority by the 21st day of the month following the month in which the deductions were made.

(d) Transactions Exempted from Withholding Tax in Nigeria:

- Direct purchase across the counter (cash sales).

- Direct purchase of raw materials from suppliers (not under contract of supply).

- Sales made in the ordinary course of business.

- Claims in insurance business;

- Interest on bonds; for and

- Dividends redistributed by holding companies.

(e) Groups Recognized as Agents for Withholding Tax Collection and Remittance:

- Corporate bodies (companies).

- Individuals, firms, and sole traders.

- Government ministries, departments, and agencies.

- Statutory bodies and public authorities.