Question

Answer

Abcee Limited

Revised income tax liability for 2016 year of assessment

Revised Tax Liability Computation under Section 19 of CITA

- Explanation of Section 19:

- Section 19 of the Companies Income Tax Act stipulates that where a company declares a dividend that exceeds its total profit as ascertained for tax purposes, the company will be assessed to tax based on the dividend declared as if it were the total profit. This is referred to as the “Dividend Tax Rule” or “Excess Dividend Tax.”

- Determine the Total Profit and Compare with Dividend Declared:

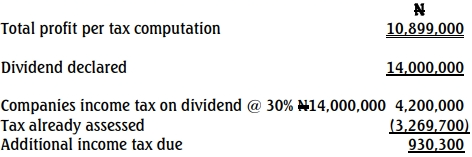

- Total profit per tax computation: N10,899,000

- Dividend declared: N14,000,000

- Application of Section 19:

- Since the dividend declared (N14,000,000) is greater than the total profit (N10,899,000), Section 19 applies, and the dividend amount will be considered as the revised total profit for tax computation.

- Compute the Revised Tax Liability:

- Revised total profit based on dividend declared: N14,000,000

- Tax rate applicable: 30%

Revised Tax Liability Calculation:

- N14,000,000 × 30% = N4,200,000

- Revised Tax Liability:

- The revised tax liability for ABCEE Limited under Section 19 is N4,200,000.

Conclusion:

The revised tax liability, in line with Section 19 of the Companies Income Tax Act, is N4,200,000, replacing the initially assessed tax of N3,269,700 based on the total profit.