Question

Answer

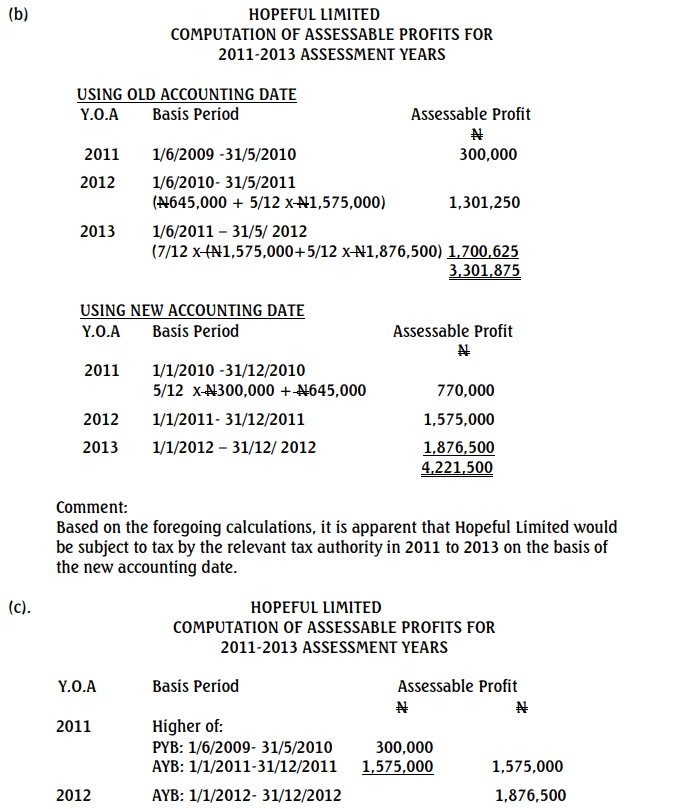

a. Steps Involved in the Event that HOPEFUL Limited Adopts the Change of Accounting Date (6 Marks)

- Board Resolution: A resolution must be passed by the Board of Directors authorizing the change of accounting year-end.

- Notification to Regulatory Authorities: Notify the Federal Inland Revenue Service (FIRS) of the change in accounting date, specifying the reasons for the change.

- Preparation of Financial Statements: Prepare financial statements covering the transitional period. This would include statements for the short accounting period from 1 June 2010 to 31 December 2010.

- Adjustments for Tax Purposes: Calculate the assessable profit for the transitional period and subsequent accounting periods based on the new year-end.

- Approval from FIRS: Obtain approval from the FIRS for the change in accounting date. This involves submitting the application along with the revised financial statements and justification.

- Amendment of Tax Returns: Amend any tax returns that may be affected by the change in accounting date, ensuring proper alignment of profits, expenses, and deductions.