Question

In the year 2000, Amotekun State of Nigeria established two State Universities University of Education (ASUE), to cater for the indigenes of the state. The following information relates to each of the universities:

a. The Bursar of Amotekun State University, Oke-Mosan, delegated the preparation of Non-current assets schedule to be included in the final accounts of the University for the year ended December 31, 2018, to one of the Deputy Bursars in the Bursary Department.

In the discharge of the assignment, the Deputy Bursar reviewed the following documents:

- International Public Sector Accounting Standards (IPSAS).

- Previous year’s financial report.

- Non-current assets register.

- Valuation reports, etc.

He was able to obtain the following information:

(i)

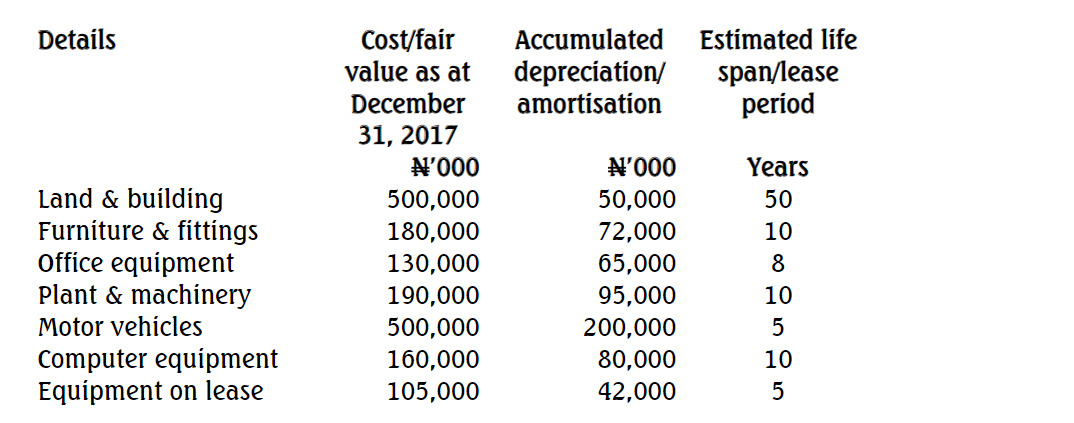

(i) It is the policy of the University to charge a full year’s depreciation on assets irrespective of the month of purchase or revaluation during the year, while no depreciation is charged on assets disposed of during the year.

(ii) Equipment on lease is depreciated equally over the period of the lease.

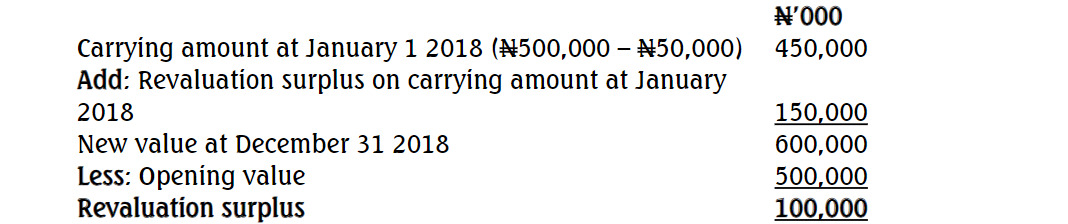

(iii) Land and buildings were professionally revalued during the year by Parisco & Associates, a firm of Chartered Surveyors and Valuers, and approved by the State Ministry of Works and Housing. The valuation, which was based on the open market value, produced a revaluation surplus of N150,000,000 over the carrying amount as at January 1, 2018.

(iv) The University purchased plant and machinery which was imported from the United Kingdom at a cost of N430,500,000. Installation and transportation costs to the University amounted to N20,500,000.

(v) The Deputy Bursar that prepared the non-current assets schedule last year classified some of the computer equipment purchased on May 15, 2017, costing N26,000,000 as office equipment. A reclassification is required in the current year.

(vi) Office furniture and fittings costing N12,250,000 were disposed of during the year for N11,500,000, which resulted in a profit of N750,000.

(vii) The University entered into an equipment lease agreement with Ode Finance Limited; the terms and conditions of the finance lease are as follows:

Principal sum: N45,000,000

Lease period: 5 years

Lease rentals: N10,000,000 p.a.

(viii) During the year, the University acquired a fleet of vehicles at the cost of N50,000,000. The State Government financed this acquisition.

Required: i. In accordance with IPSAS 13, identify FIVE features of a finance lease. (5 Marks) ii. Prepare the non-current assets schedule of Amotekun State University suitable for publication. (15 Marks)

Answer

a. i. In accordance with IPSAS 13, the following are the features of a finance lease:

- Ownership is transferarble to the lessee.

- Risks and rewards incidental to ownership reside with the lessee.

- Option to purchase the asset at a lower value than the fair value.

- The lease term is for the major part of the economic life of the assets even if ownership is not transferred.

- At the inception of the lease, the present value of the minimum lease payments amounts substantially to at least, the fair value of the leased assets.

- The lease assets are of such a specialised nature that only the lessee can use them without major modifications.

- The lease assets cannot easily be replaced by other assets.

- If the lessee can cancel the lease, the losses associated with the cancellation are born by the lessee.

- The lessee has the ability to continue the lease for a secondary period at a rent substantially lower than the market rent.

- Gains or losses from the fluctuations in the fair value of the residual assets should accrue to the lessee.

ii. Amotekun State University

Non- current asset schedule

Workings:

i Revaluation of land and buildings

ii. Depreciation

iii. Depreciation on leased equipment

iv. Depreciation on asset disposed