- 20 Marks

Question

The trial balance for Odum Ltd. as at 31 December 2021 is as follows:

| Account | Dr (GHȼ) | Cr (GHȼ) |

|---|---|---|

| Sales revenue | 377,615 | |

| Purchases | 130,006 | |

| Inventory as at 1 January 2021 | 60,890 | |

| Insurances | 5,678 | |

| Salaries | 61,600 | |

| Electricity | 4,250 | |

| General expenses | 8,663 | |

| Allowance for receivables | 540 | |

| Land and Buildings at cost | 80,000 | |

| Buildings accumulated depreciation | 21,500 | |

| Machinery at cost | 65,000 | |

| Machinery accumulated depreciation | 12,400 | |

| Fixtures and fittings at cost | 24,000 | |

| Fixtures and fittings accumulated depreciation | 9,600 | |

| Trade receivables | 64,500 | |

| Trade payables | 14,062 | |

| Bank | 20,110 | |

| Ordinary shares | 50,000 | |

| Retained earnings as at 1 January 2021 | 15,480 | |

| 10% Loan | 25,000 | |

| Loan interest | 1,500 |

(Dr Total: 526,197 GH¢ / Cr Total: 526,197 GH¢)

Additional Information:

- Inventory at 31 December 2021 amounted to GHȼ80,000. Some goods sent out on a sale or return basis have been treated as credit sales. These goods cost GHȼ6,000 and had been invoiced to the customer for GHȼ7,500. The customer has informed the company that it now intends to return these goods.

- The balance shown for salaries covers the 11 months to 30 November 2021. Salaries for December 2021 are due and unpaid. There have been no salary increases over the previous 12 months, and an equal amount is paid each month.

- Insurances include GHȼ660 for the half-year ended on 31 March 2022.

- Dividends paid during the year of GHȼ2,700 have been credited to bank and debited to General expenses.

- The loan was obtained in August 2018 and is repayable in full during the financial year ended 31 December 2023.

- Depreciation is to be provided on all machinery at 15% per annum using the reducing balance method. Machinery costing GHȼ15,000 was purchased on 1 July 2021, and this is included in the balance shown for machinery. Depreciation is calculated for each proportion of the year for which machinery is held. There were no disposals of machinery during the year.

- All the fixtures and fittings were purchased for GHȼ24,000 on 1 January 2019. Depreciation is to be charged using the straight-line method.

- Buildings are to be depreciated by GHȼ3,500 for the year. Land is not depreciated.

- Allowance for receivables is to be provided as GHȼ2,400 for a specific debt, plus 4% on the remainder of receivables.

- Taxation for the year is estimated as GHȼ42,012.

(Note: Revenue and expenses are deemed to accrue evenly throughout the year)

Required:

Prepare, for Odum Ltd, the following statements in accordance with International Financial Reporting Standards (IFRS).

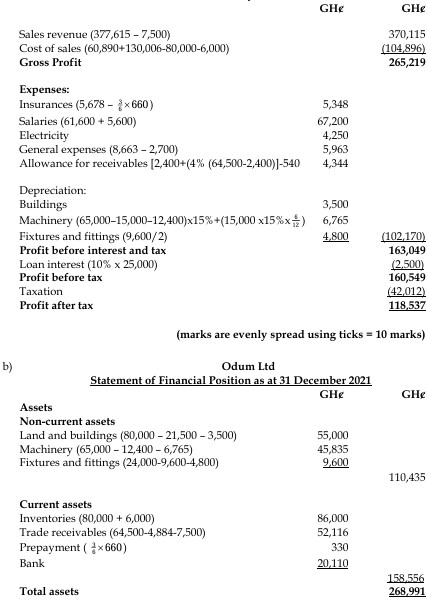

a) The Statement of Profit and Loss for the year ended 31 December 2021. (10 marks)

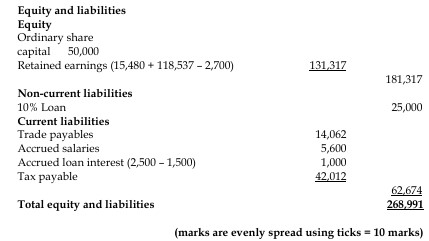

b) The Statement of Financial Position as at 31 December 2021. (10 marks)

Answer

a) Odum Ltd. – Statement of Profit and Loss for the year ended 31 December 2021

- Uploader: Theophilus