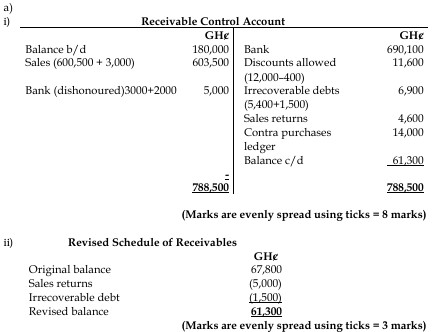

Question

Answer

b) Books of Prime Entry:

- Sales Day Book:

- Records credit sales transactions. This book captures details of sales made to customers on credit, including the date, customer name, sales amount, and relevant accounts affected.

- Purchases Day Book:

- Records credit purchases transactions. It records purchases made on credit, including the date, supplier name, purchase amount, and relevant accounts impacted.

- Cash Book:

- Records cash receipts and payments. It records all cash transactions, including cash receipts from customers, cash payments to suppliers, and other cash-related activities.

- General Journal:

- Records non-routine or adjusting entries. It is used for transactions that cannot be recorded in the other specialized journals. This includes adjusting entries, corrections, and any other miscellaneous transactions.

- Sales Return Day Book:

- Records returns of goods by customers. This journal captures details of goods returned by customers, including the date, customer name, return amount, and relevant accounts affected.

- Purchases Return Day Book:

- Records returns of goods to suppliers. It records details of goods returned to suppliers, including the date, supplier name, return amount, and relevant accounts impacted.

- Petty Cash Book:

- Records routine or unexpected petty or small cash payments.

(6 day books well explained @ 1.5 marks each = 9 marks)