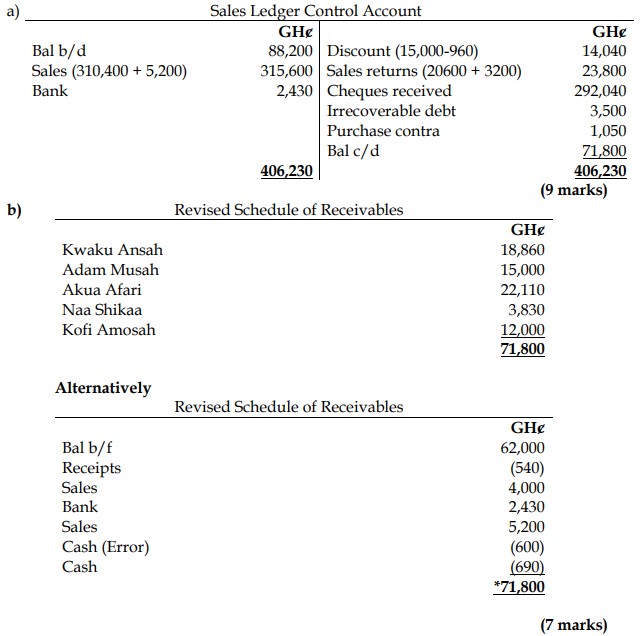

Question

Answer

c)

Usefulness of Control Accounts to Businesses

- Error Detection and Correction:

Control accounts help identify discrepancies between the general ledger and subsidiary ledgers, making it easier to locate and correct errors. This process enhances the accuracy of financial records. - Fraud Prevention and Detection:

By providing an independent check on the sales ledger and purchases ledger, control accounts serve as a deterrent against fraud. They ensure that any discrepancies are quickly identified, reducing the risk of fraudulent activities.

(4 marks evenly spread)