Question

Answer

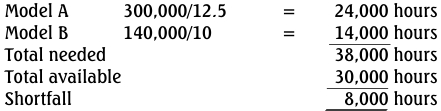

a. The machine hours are insufficient to produce all the budgeted quantity:

Hours needed:

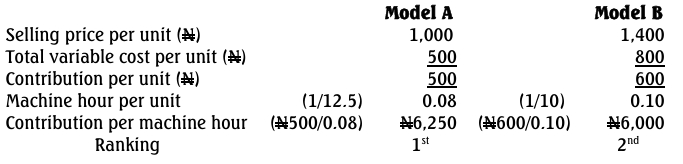

Calculation of contribution and ranking

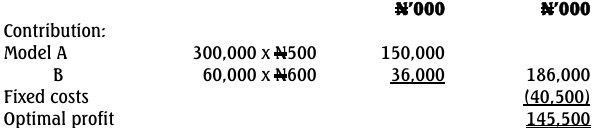

Calculation of optimal production plan

![]()

The company should therefore produce 300,000 units of Model A and 60,000

units of Model B.

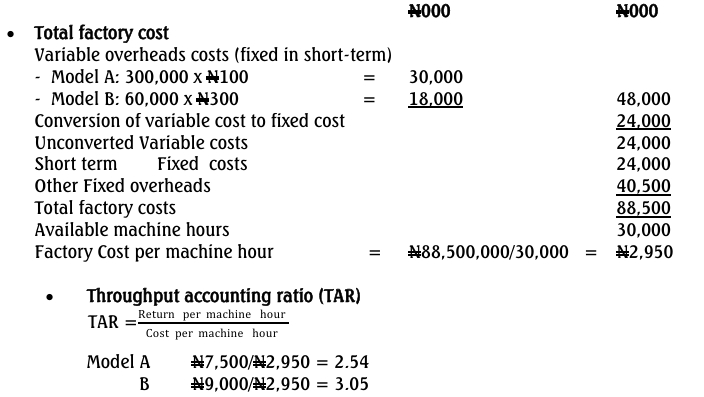

Calculation of projected profit

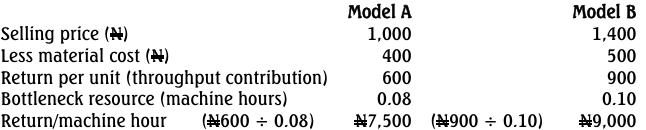

b. Throughput accounting ratio = return per factory hour/cost per factory hour

Return per factory hour = Sales – material costs/usage of bottleneck resource

Cost per machine hour = Total factory cost/Total available machine hours

Recommendation: Products with a TAR greater than 1.0 are worth producing, as the throughput return per hour exceeds the cost per factory hour.

c. Since Model B has a higher return per machine hour than Model A, PK Ltd should produce Model B until it has satisfied the total demand for 140,000bunits. The production mix will therefore be as follows:

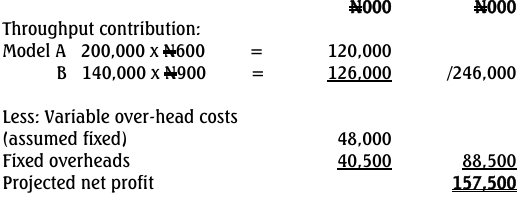

Calculation of projected profit

d. Differences in ‘Contribution’ in Throughput Accounting vs. Marginal Costing

- Variable Costs Considered: Throughput accounting only considers direct material costs as variable, while marginal costing includes direct labor and variable overheads in the calculation of contribution.

- Inventory Focus: Throughput accounting aligns with Just-in-Time philosophy, valuing only materials purchased for immediate production, while marginal costing may include material costs based on usage within the period, irrespective of timing in the production cycle.