Question

Answer

a) Garki Plc

b)

Assumption: External offer price from intermediate market from Beta Division is

equal to or greater than N4.95 transfer price.

c. Sub-optimal decision-making:

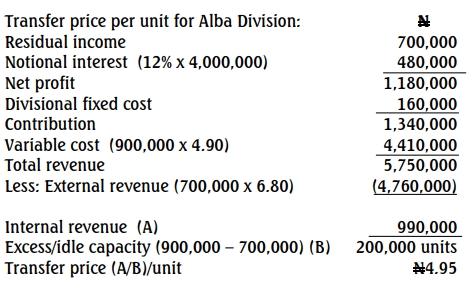

The transfer price of N4.95 may lead to sub-optimal decision-making from Garki plc’s overall perspective because Alba Division could sell the same component externally for N6.80, resulting in a loss of N1.85 per unit for internal transfers. Additionally, fixed costs and mark-up in Alba Division’s pricing lead Beta Division to incur a higher input cost, affecting overall profitability.

d. Negotiated transfer price versus market-based price:

A negotiated transfer price is appropriate when there is no perfect external market for the component or when divisions within the group have conflicting objectives. It allows managers to reach a mutually beneficial agreement, ensuring autonomy. On the other hand, a market-based transfer price is used when an external market exists, simplifying the pricing process by using the prevailing market rate.