Question

Answer

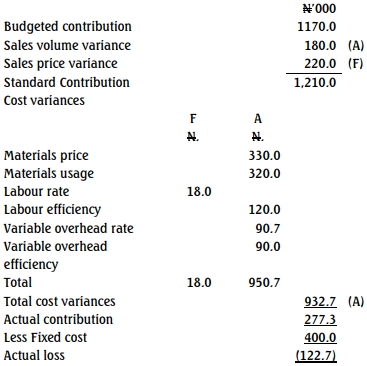

(a) Reconciliation Statement between Budgeted and Actual Profit

Workings

TOMA PASTE NIGERIA LIMITED

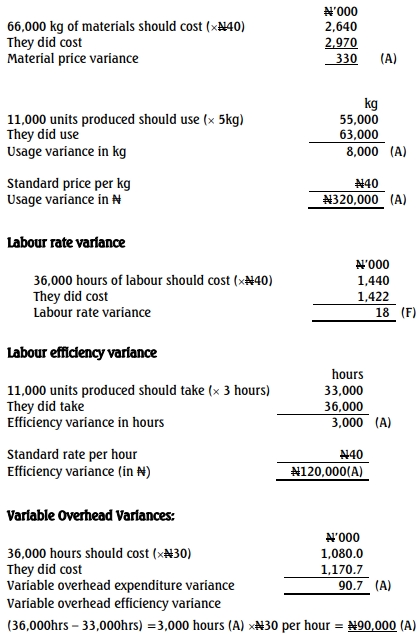

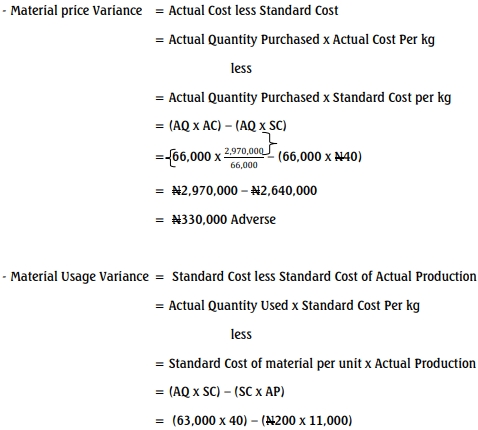

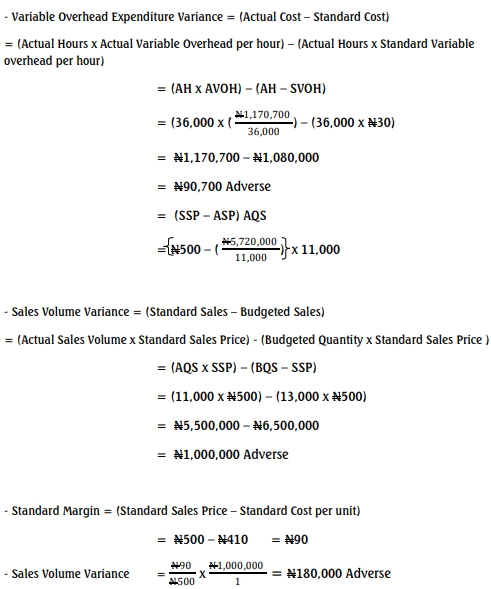

Materials price variance: based on quantities purchased since inventories are

valued at standard cost.

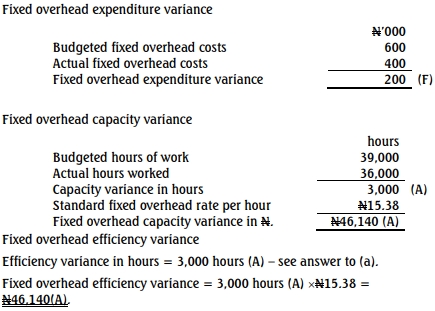

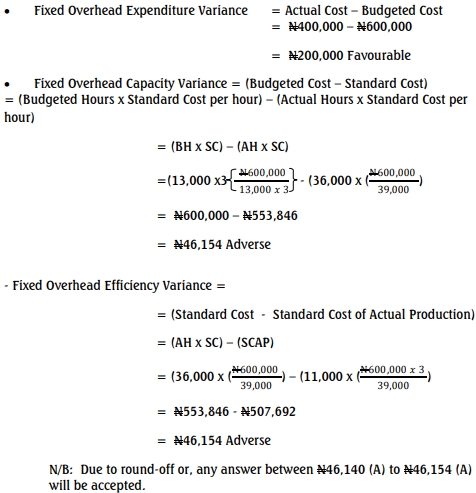

ALTERNATIVE TO COMPUTING VARIANCES

If the company uses absorption costing with a direct labour hour absorption

rate, we can calculate an expenditure, capacity and efficiency variance for

fixed production overheads.

Budgeted absorption rate per hour:

Budgeted labour hours: 13,000 x 3 = 39,000 hrs

Budgeted fixed cost N600,000

Budgeted absorption rate: N600,000 /39,000 = N15.38

ALTERNATIVE SOLUTION

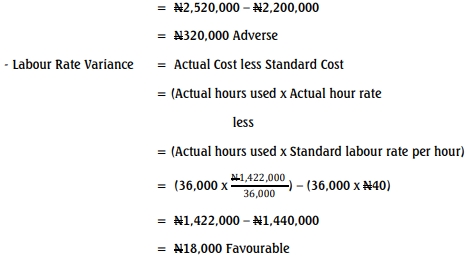

(c) Labour rate

The labour rate variance is favourable indicating a lower rate per hour was

paid than expected. This is perhaps because lower grade of labour were

used during production. Though less likely, it is possible that staff had a

pay cut imposed upon them/decrease in buy rate. Finally, an incorrect or

outdated standard could have been used.

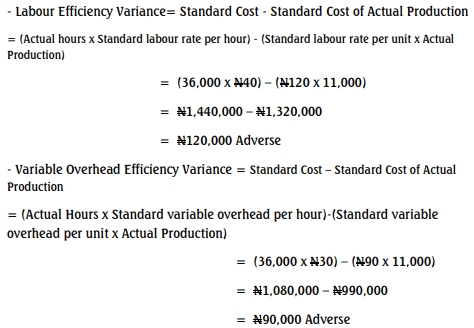

Labour efficiency

This is significantly adverse, indicating staff took much longer than

expected to complete the output. This may relate to the favourable labour

rate variance, reflecting employment of less skilled or experienced staff.

Staff demotivated by a pay cut are also less likely to work efficiently.

It may also relate to the reliability of machinery as staff may have been

prevented from reaching full efficiency by unreliable equipment. Others

include:

- Decrease in machine set up time

- Idle time

- Lack of motivation

- Faulty equipment/Machine breakdown