Question

Answer

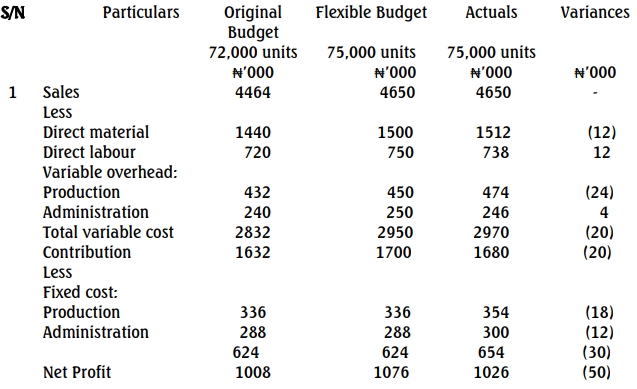

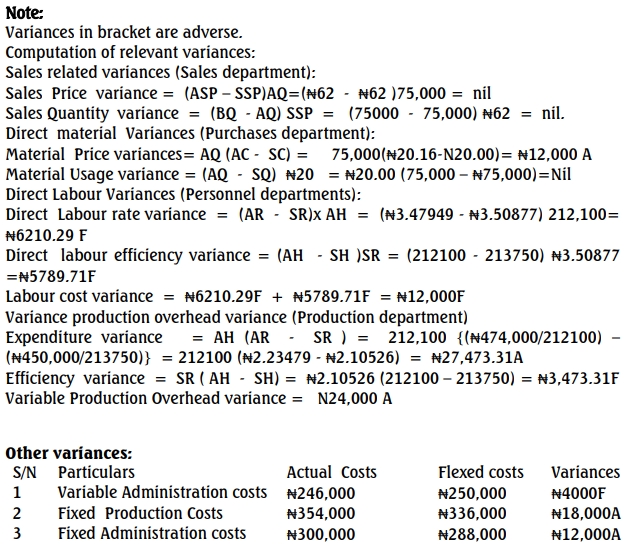

a. Redrafted Budget Statement

The redrafted statement will highlight key areas where the budget has either been over- or under-spent. Variances should also be classified as favorable or unfavorable to better understand the department’s financial performance.

b. Behavioral Problems Associated with Budgeting

- Perceived Unfairness: Employees may feel that the budget system is used as a tool for criticism, which creates distrust and resentment, as demonstrated by Mr. Okoli’s reaction.

- Lack of Understanding: The rushed implementation and inadequate explanation of the budget system has left managers, like Mr. Okoli, feeling alienated and skeptical about its validity.

- Pressure to Perform: Budgeting can create excessive pressure to meet financial targets, leading to low morale and disengagement from the budgeting process.

- Misalignment with Departmental Goals: The budget may not reflect the real operational conditions or specific challenges faced by departments, leading to frustration among department heads.

c. Recommendations for Improvement

- Provide Adequate Training: Educate department heads on how the budget system works and ensure they understand the rationale behind it, thus fostering greater buy-in.

- Involve Managers in the Budgeting Process: Include department heads in the creation of their budgets to ensure alignment with departmental goals and operational realities.

- Focus on Realistic Targets: Ensure that the budget targets are achievable and reflect the current economic and operational environment to reduce pressure and boost morale.

- Implement Rolling Budgets: Rather than relying on fixed budgets, rolling budgets should be considered to allow for adjustments based on changing market and operational conditions.