Question

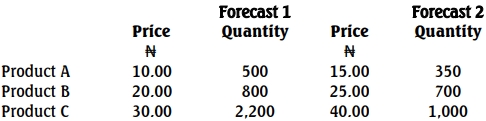

PQR Plc is preparing its budgets for the upcoming year and has forecasted two demand scenarios for its product range:

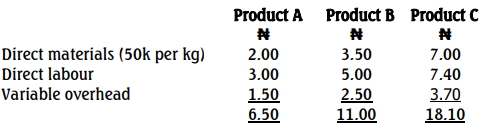

You are to assume only one forecast (either Forecast 1 or Forecast 2) will be selected. The expected variable unit costs for each product are:

The general fixed costs are budgeted at ₦20,000 for the year, with no specific fixed costs expected per product. Additionally, all three products use the same direct material, with a limited supply of 22,020 kgs available for the budget year.

Required:

a. Recommend, with supporting calculations, whether forecast 1 or forecast 2 should be adopted for the budget period. (11 Marks)

b. Prepare a report, addressed to the managing director, to explain the budget preparation process, with particular reference to: i. The principal budget factor (3 Marks)

ii. The budget manual (3 Marks)

iii. The role of the budget committee (3 Marks)

Answer

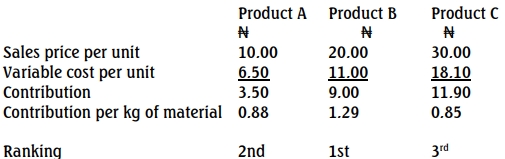

a. Materials supply is a limiting factor for forecast 1, but not for forecast 2.

Forecast 1

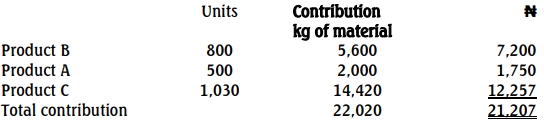

Optimal production plan for forecast 1

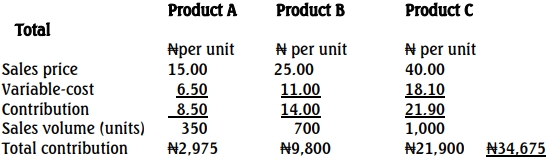

Optimal Production Plan for forecast 2

Recommendation: Forecast 2 should be adopted for the budget period as it provides a total contribution of ₦34,675, which is ₦13,468 higher than Forecast 1)

b. Report to the Managing Director on Budget Preparation Process

To: Managing Director

From: Finance Manager

Subject: Budget Preparation Process

Date: May 5, 2021

- Introduction:

This report addresses key issues in the budget preparation process as requested by PQR Plc. - Principal Budget Factor:

The principal budget factor, also known as the limiting factor, is a constraint that affects planning limitations within the organization, such as limited material supply, staffing, or financial resources. For PQR Plc, material availability is the limiting factor for the selected forecast. - Budget Manual:

The budget manual provides guidelines and instructions from the Budget Committee to guide departmental heads in preparing budgets. It ensures alignment with organizational goals, consistency in estimation, and a structured approach to budgeting. - Role of the Budget Committee:

The Budget Committee comprises senior management, including the CEO, heads of business units, and the CFO, responsible for overseeing budget preparation, setting budget goals, approving final budgets, monitoring budgetary compliance, and recommending adjustments as necessary. This committee plays a vital role in aligning budgetary goals with strategic objectives, analyzing variances, and ensuring financial discipline .