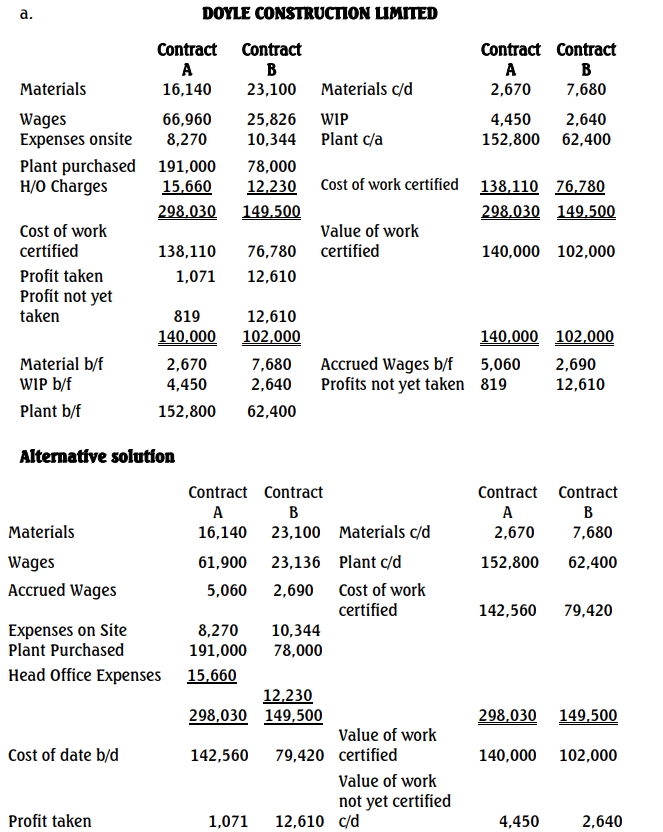

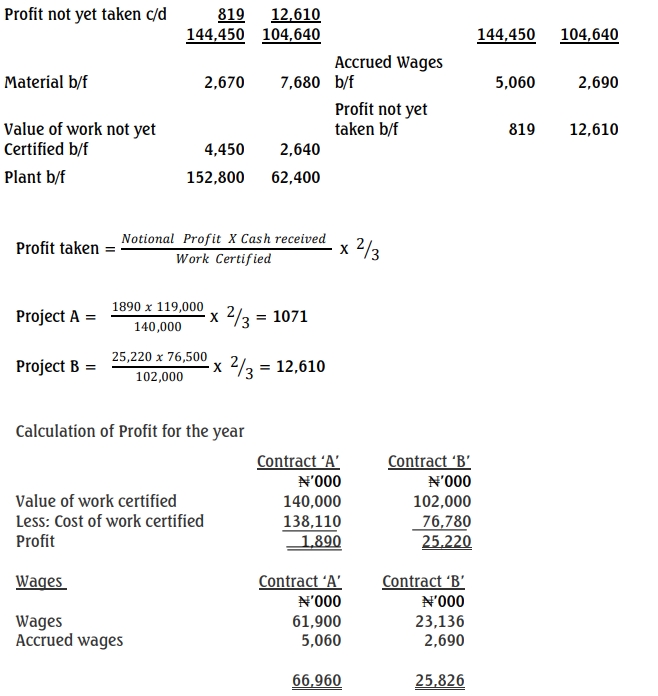

Joyle Construction Limited is currently working on two contracts with the following details as at December 31.

Details

Contract A (₦’000)

Contract B (₦’000)

Material

16,140

23,100

Wages

61,900

23,136

Expenses on site

8,270

10,344

Plant purchased

191,000

78,000

Accrued wages

5,060

2,690

Materials as at 31/12

2,670

7,680

Value of work certified

140,000

102,000

Cash received on certified work

119,000

76,500

Completed work not yet certified

4,450

2,640

Head office charges apportioned

15,660

12,230

Plant value as at 31/12

152,800

62,400

The contract value is ₦500,000,000 for Contract A and ₦350,000,000 for Contract B.

Required:

Prepare contract “A” and contract “B” accounts for Joyle Construction Limited as at December 31 in a columnar form. Show the profit taken at year-end and the balances carried forward. (Show workings where necessary).