Question

Answer

a)

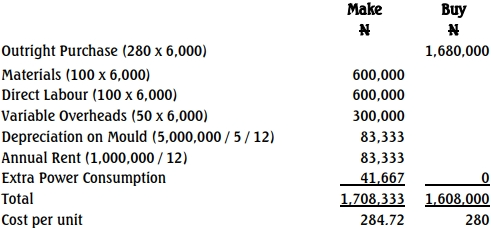

SEAGULL FABRICATORS LIMITED

COMPARATIVE STATEMENT (MONTHLY)

Based on the figures above, the company is advised to continue purchasing the component rather than in-house fabrication. It is cheaper to outsource.

b)

i. Qualitative Factors to Consider Before Outsourcing

- Quality of the Product: Ensuring the outsourced product meets the required quality standards.

- Reliability of the Supplier: The consistency and dependability of the supplier in delivering components on time.

- Impact on Workforce: Potential job losses or changes in roles for employees if production is outsourced.

ii. Quantitative Factors to Consider

- Cost Comparison: Total cost of in-house production versus the cost of outsourcing.

- Break-Even Analysis: Analysis of the point at which in-house production becomes more cost-effective than outsourcing.

- Investment in Fixed Assets: The cost of purchasing new equipment or infrastructure required for in-house production.