Question

Answer

a. The purpose of diluted EPS measures is to provide a warning to investors about potential decreases in EPS if all possible shares were issued. It represents the maximum potential dilution of current EPS, reflecting hypothetical share issuance scenarios under the most dilutive conditions. The three types of dilution are:

- Convertible Instruments: Adjust earnings for saved interest (net of tax) and adjust shares for the increase due to conversion.

- Options to Acquire Ordinary Shares: Adjust shares for the effect of share options or warrants, reflecting the number issued at no consideration.

- Contingently Issuable Shares: Include shares that could be issued based on future earnings or other performance metrics if criteria are met.

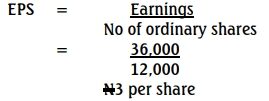

b. Basic Earning Per Share (EPS) for the year ended December 31, 2022

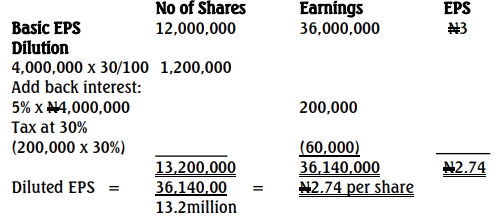

Diluted EPS for the year ended December 31, 2022

c. Conditions for Alternative EPS:

- A reconciliation of the alternative EPS with the amount in the statement of profit or loss.

- The alternative EPS must use the same weighted average share number as IAS 33 calculations.