Question

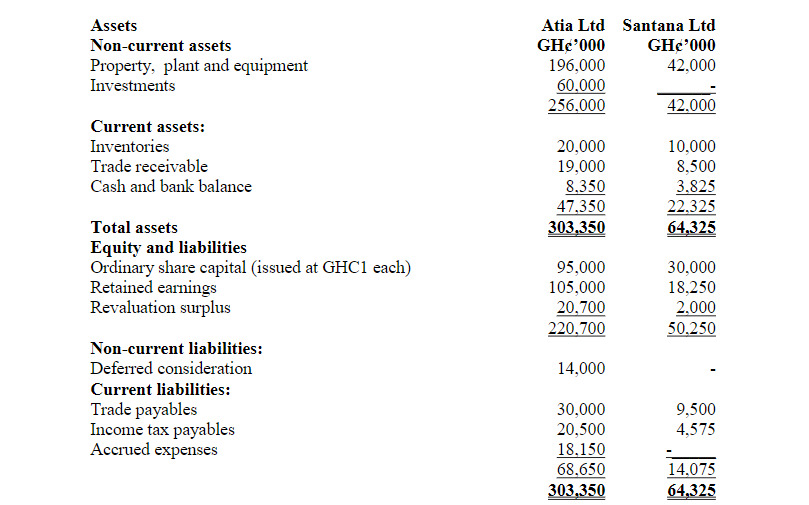

The draft statements of financial position of Atia Ltd and that of Santana Ltd as at 30 June 2019 are as follows:

Additional relevant information:

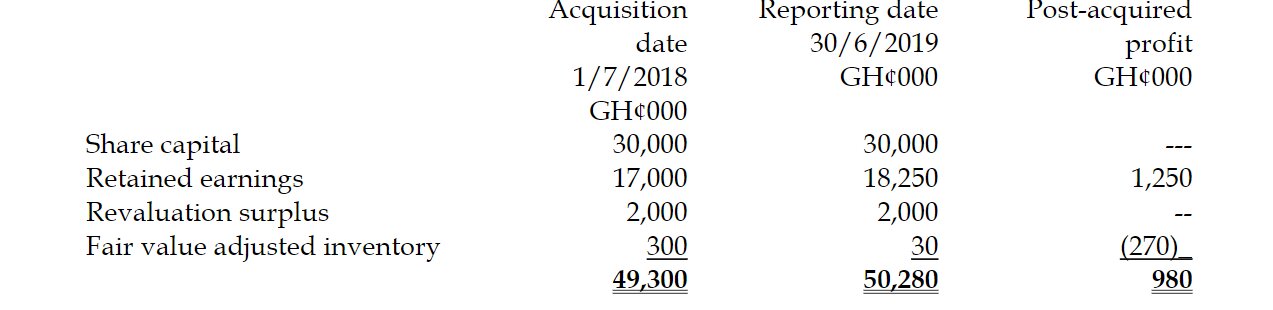

1) On July 1, 2018, Atia Ltd purchased 21 million shares of Santana Ltd. At this date, the retained earnings of Santana Ltd were estimated at GH¢17 million, and the revaluation surplus was GH¢2 million.

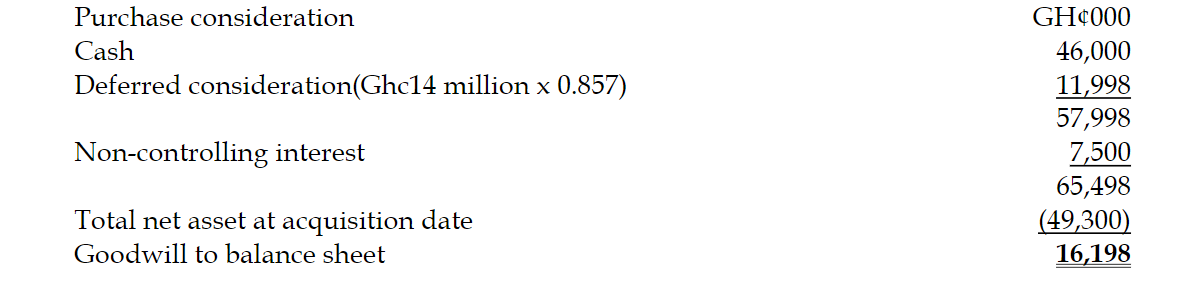

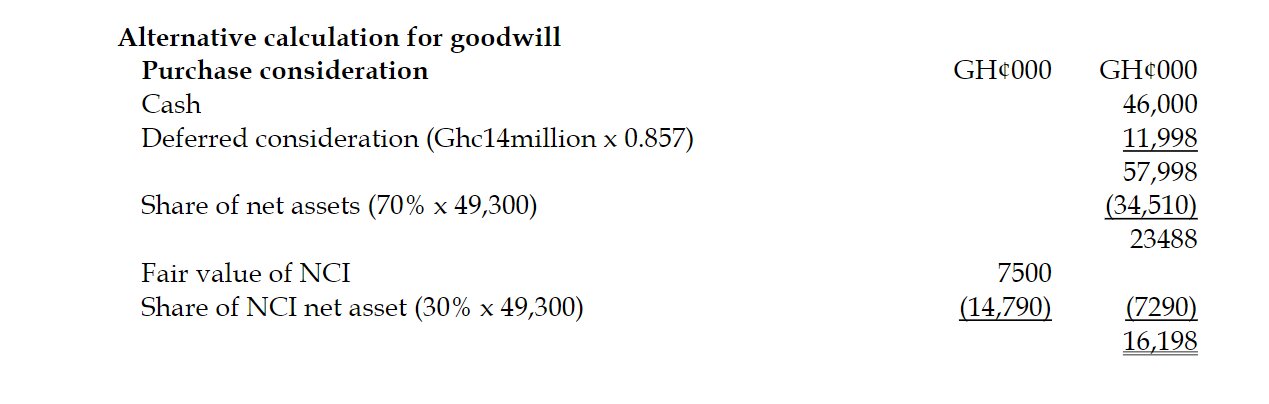

2) Atia Ltd paid an initial cash amount of GH¢46 million and agreed to pay Santana Ltd’s shareholders a further GH¢14 million on July 1, 2020. The financial accountant has recorded both elements of the consideration in investments.

3) Atia Ltd has a cost of capital of 8% per annum.

4) During the accounting period, Atia Ltd sold goods totaling GH¢4 million to Santana Ltd at a gross profit margin of 25%. As of 30 June 2019, Santana Ltd still had GH¢0.5 million of these goods in inventory. Atia Ltd has a normal margin of 45%.

5) On the acquisition date, the fair values of Santana Ltd’s net assets were equal to their carrying amounts, except for inventory, which had a cost of GH¢1.5 million but a fair value of GH¢1.8 million. As of 30 June 2019, 10% of these goods remained in Santana Ltd’s inventory.

6) Atia Ltd values non-controlling interest (NCI) at fair value. The NCI’s value at acquisition is estimated at GH¢7.5 million.

7) No impairment was recognized for goodwill.

Required: Prepare the consolidated statement of financial position of the Atia group as at 30 June 2019.

(20 marks)

Answer

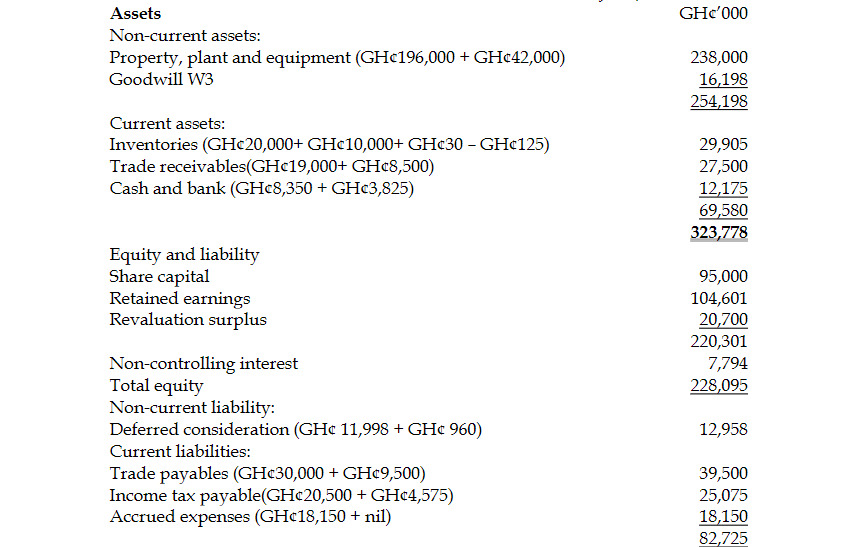

Atia group

Consolidated Statement of Financial Position as at 30 June, 2019

Atia Ltd’s investment in Santana Ltd (70%):

Or

b)

Date of reporting 30 June 2019

Acquisition Date 01 July 2018

Post-acquisition period 1 year

2. Net assets of Santana

3. Goodwill

4. Non-controlling interest (NCI):

Fair value of NCI: GH¢7,500

Share of post-acquisition profit (30% × GH¢980): GH¢294

Total: GH¢7,794

5. Group Retained Earnings:

Atia Ltd retained earnings: GH¢105,000

Share of post-acquisition profit (70% × GH¢980): GH¢686

Unwinding discount on deferred consideration (GH¢11,998 × 8%): GH¢(960)

Unrealized profit (25% × GH¢500): GH¢(125)

Total: GH¢104,601