Question

Answer

i. Treatment of the Property in the Financial Statements (Compliance with IAS 40):

- The property should be classified as investment property because the majority of the floor space (approximately 94%) is rented out to third parties for earning rental income, which meets the definition of investment property under IAS 40.

- Although part of the building (6%) is used as an administrative office, IAS 40 allows the entire property to be classified as investment property since the portion used for administrative purposes is insignificant and the property cannot be sold separately.

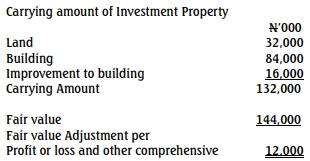

- The property should be measured using the fair value model, as per the company’s policy. The fair value as at December 31, 2014, determined by the independent valuer, is N144,000,000.

- Repairs and maintenance expenses (N2,000,000) should be recognized in the statement of profit or loss as an operating expense.

- Rental income (N6,400,000) should also be recognized in the statement of profit or loss as income.

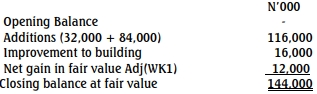

ii. Calculation of the Value of Investment Property:

WORKINGS