Question

Answer

a:

Discussion of two measurement models for intangible assets:

- Cost Model:

Under the cost model, an intangible asset is carried at its cost less any accumulated amortization and impairment losses. This model is commonly used when there is no active market for the intangible asset to reference for fair value. Amortization is charged over the asset’s useful life unless the asset has an indefinite life, in which case it is tested for impairment annually. - Revaluation Model:

In the revaluation model, an intangible asset is carried at a revalued amount, being its fair value at the date of revaluation less any subsequent accumulated amortization and impairment losses. This model can only be applied if there is an active market for the intangible asset. Revaluations are done regularly to ensure the carrying amount does not differ significantly from fair value.

b:

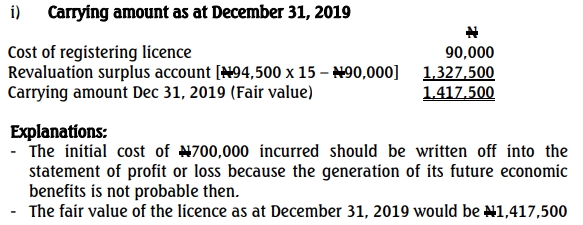

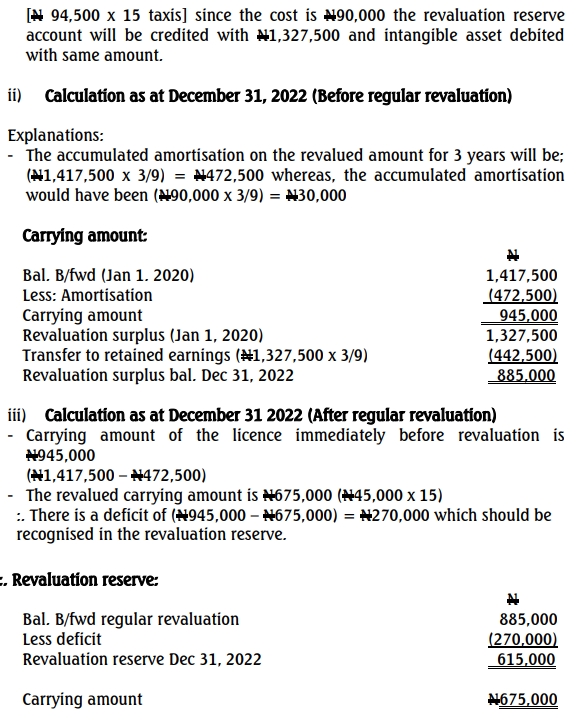

Calculation and explanation of the carrying amount and revaluation surplus of Olumo-Taxi Limited’s intangible assets