Question

Lamido Limited is a courier service company that operates in Nigeria and West Africa.

Initially, Lamido Limited experienced strong growth, but in recent periods the company has been criticised for under-investing in its non-current assets.

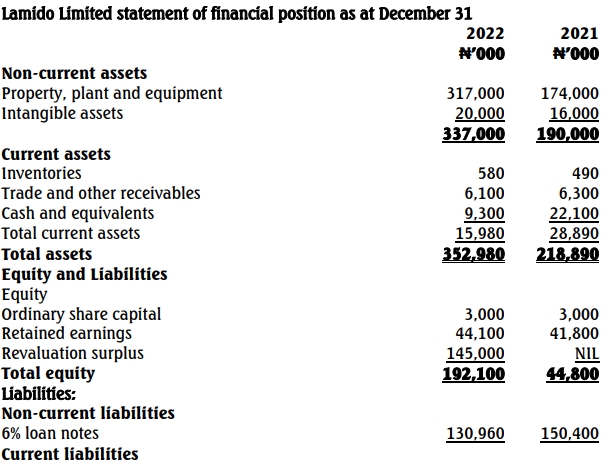

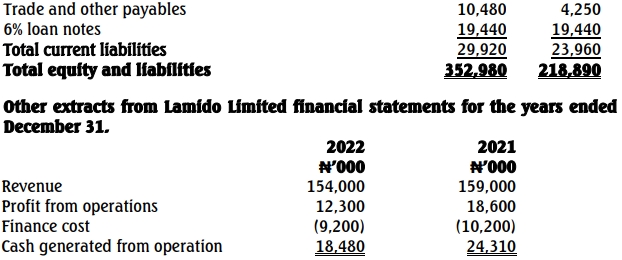

Lamido Limited statement of financial position as at December 31:

The following information is also relevant:

- Lamido Limited had exactly the same delivery volumes in 2022 as in 2021, with the customer base being the same in both years.

- In October 2022, Lamido Limited had to renegotiate its operating licenses in three of its countries of operation. This led to an increase in the fees Lamido Limited had to pay to operate in these countries. The operating licenses in five other countries are due to expire in December 2022, and Lamido Limited is currently negotiating with the concerned authorities of these countries.

You are required to:

a. Calculate the following ratios for the years ended December 31, 2021, and 2022:

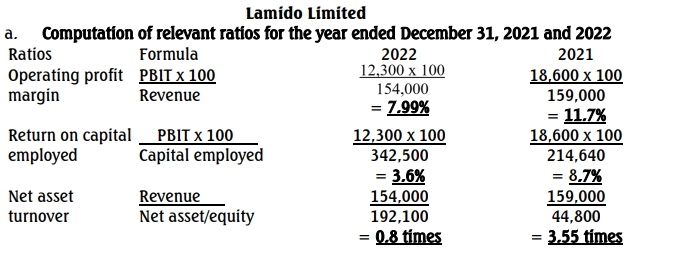

i. Operating profit margin

ii. Return on capital employed

iii. Net asset turnover

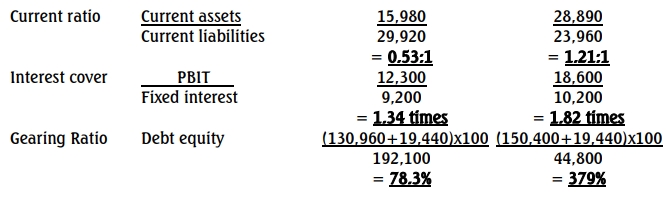

iv. Current ratio

v. Interest cover

vi. Gearing (Debt/equity)

(6 Marks)

b. Comment on the performance and position of Lamido Limited for the year ended December 31, 2022, and highlight any issues Lamido Limited should consider in the near future. (14 Marks)

Answer

b:

Comments on performance and position of Lamido Ltd for the year ended December 31, 2022:

Performance:

- Revenue: Lamido Ltd’s revenue declined slightly from ₦159,000,000 in 2021 to ₦154,000,000 in 2022. Although the volume of deliveries remained constant, the drop in revenue could be due to price reductions or increased competition.

- Operating profit margin: The operating profit margin decreased significantly from 11.7% in 2021 to 7.99% in 2022. This indicates that the company’s profitability has been impacted by rising costs, particularly the renegotiated operating licenses and possibly higher fixed costs.

- Return on capital employed (ROCE): ROCE fell sharply from 8.7% to 3.6%, reflecting both a decline in profits and the revaluation of assets in 2022. The significant revaluation increased capital employed, leading to a lower return.

- Interest cover: The interest cover ratio has declined from 1.82 times to 1.34 times, indicating that Lamido Ltd is increasingly constrained in covering its finance costs with operating profits. This may signal potential liquidity concerns, especially given the level of debt in the company.

Position:

- Net asset turnover: The company’s efficiency in generating revenue from its assets has deteriorated, as shown by the drop in the net asset turnover ratio from 3.55 times to 0.8 times. This was heavily impacted by the revaluation surplus of ₦145,000,000 added to equity, inflating the net assets figure.

- Current ratio: Lamido Ltd’s liquidity position has weakened significantly, with the current ratio dropping to 0.53:1 from 1.21:1. This indicates that the company may struggle to meet its short-term obligations, as its current liabilities far exceed its current assets.

- Gearing: The company’s gearing ratio has improved from 379% to 78.3%, largely due to the revaluation surplus, which boosted equity. However, the company is still highly leveraged, and the high level of debt could pose a risk if cash flows do not improve to cover finance costs and debt repayments.

Issues to consider:

- Debt repayment: Lamido Ltd is highly reliant on debt financing, and with loan notes totaling ₦150,400,000, the company needs to carefully manage its cash flows to ensure it can meet its debt obligations. Failure to do so could lead to financial distress.

- Operating licenses: The renegotiation of operating licenses has increased costs in three countries, and similar cost increases could occur in the other five countries where licenses are due for renewal. This may put further pressure on profitability.

- Asset investment: While Lamido Ltd has revalued its non-current assets, the criticism regarding under-investment remains valid. The company may need to invest more in non-current assets to maintain and grow its operational capacity, especially given the competitive nature of the courier industry.