Question

Answer

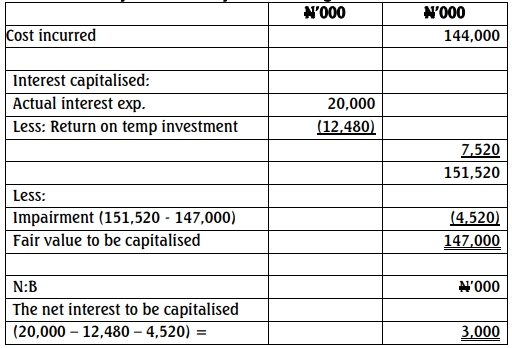

Amount to be capitalised in respect of building

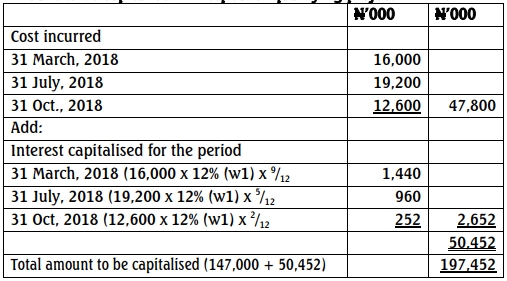

Amount to be capitalised in respect of qualifying project

Amount to be capitalised in respect of building

Amount to be capitalised in respect of qualifying project