Question

Answer

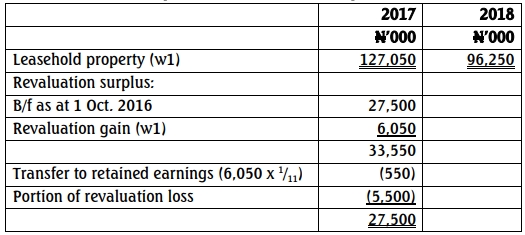

Extract of Statement of Profit or Loss for the Year Ended 30 September

| 2017 | N’000 |

|---|---|

| Amortization | (11,000) |

| Revaluation Gain | 6,050 |

| 2018 | N’000 |

|---|---|

| Amortization | (11,550) |

| Revaluation Loss | (13,750) |

Statement of financial position extract as at 30 September