Question

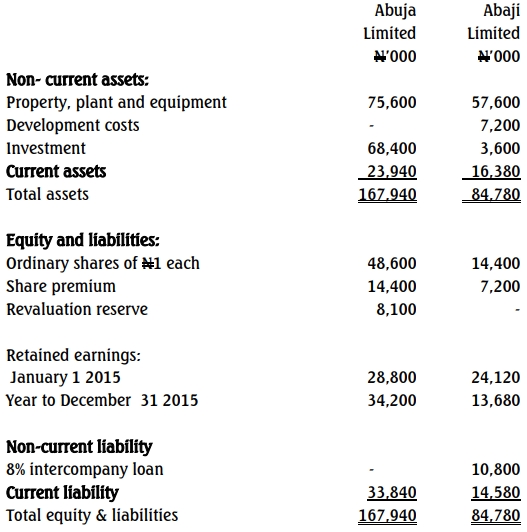

Abuja Limited acquired 80% of Abaji Limited’s ordinary shares on January 1, 2015. The company paid an immediate N5.00 per share and a further payment of N19,440,000 in cash. The company only recorded the cash consideration of N5 per share. The two statements of financial position as of December 31, 2015, are as follows:

Additional Information:

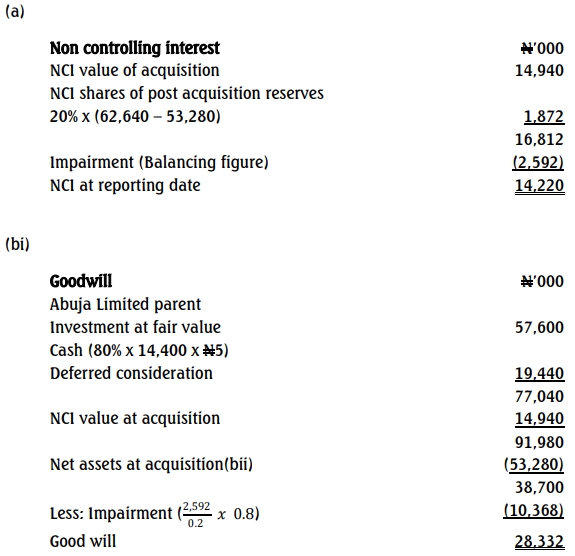

- Non-Controlling Interests (NCI): Abuja Limited values NCI using the fair value at the acquisition date, set at N14,940,000. Due to impairment, the NCI value reduced to N14,220,000 by December 31, 2015.

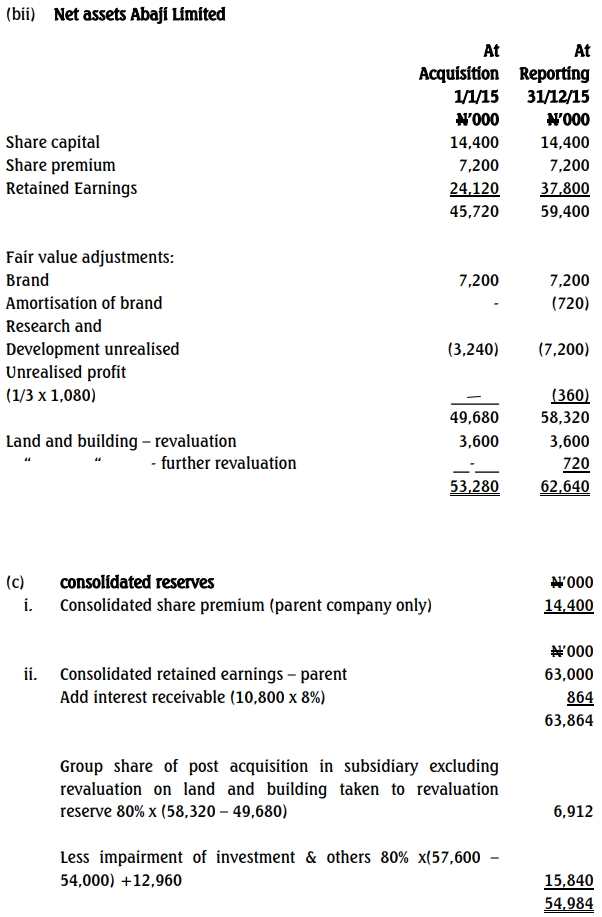

- Revaluation: Abaji Limited revalued its land and buildings at the acquisition date, increasing the value by N3,600,000, with an additional increase of N720,000 on December 31, 2015.

- Brand Valuation: Abaji Limited’s product line brand was valued at N7,200,000, with a 10-year useful life as of January 1, 2015. This brand is not included in Abaji’s statement of financial position.

- Intercompany Loan: Abuja Limited provided a loan of N10,800,000 to Abaji Limited at acquisition. Interest, payable annually, was not recorded by Abuja Limited by the end of the year.

- Development Costs: Abaji Limited completed a development project on June 30, 2015, costing N9,000,000, of which N1,800,000 was amortized by year-end. Only N3,240,000 of development costs were capitalized by the acquisition date, but Abuja Limited’s directors deem these costs unrecognized assets under IAS 38.

- Inventory Profits: Abaji Limited sold goods to Abuja Limited, with one-third remaining in Abuja’s inventory at December 31, 2015. The sale profit was N1,080,000.

Required:

Provide the figures to be included in the consolidated statement of financial position as of December 31, 2015, for:

- a. Non-Controlling Interest (7 Marks)

- b. Goodwill (7 Marks)

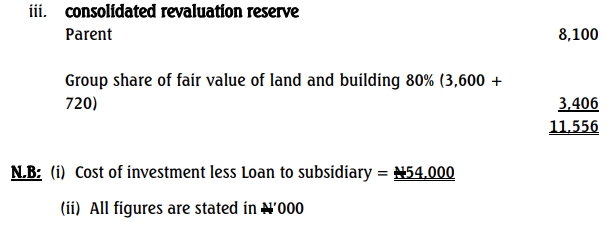

- c. Consolidated Reserves:

i. Share premium

ii. Retained earnings

iii. Revaluation reserve

(Show workings for all calculations)

Answer