Question

Answer

i. In accordance with IAS 8, Accounting policies, changes in accounting

estimate and correction of prior period errors, a change in accounting

estimate involves a change in the periodic consumption of assets which is

similar to the case of Oluwaseun Plc. In line with IAS 8, a change in

accounting estimate should be applied prospectively i.e from the year of

change and in future periods. In addition, IAS 16 – Property, Plant and

Equipment states that when an entity changes its depreciation method and

useful live such should be treated as a change in accounting estimate and

the current and future years depreciation should be based on the carrying

amount of the asset at the date of the change.

Drawing from the above, the assistant accountants’ suggestion of crediting

the income statement with an amount debited from accumulated

depreciation is not acceptable and not in line with IAS 8 and 16.

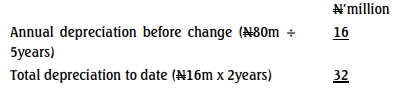

By applying IASs 8 and 16, the carrying amount in the date of the change i.e 1st

October 2014 is derived as follows:

Therefore carrying amount at 1/10/2014 = N80m – N32m = N48m

So, for the year ended 30 September 2015, the depreciation charge will be

N48m divided by 6 (i.e the revised useful life of 8 less the already used up

life of 2 years). This depreciation charge should be a charge against profit or

loss for the current period and in future periods until a more reliable useful

life is determined.

In conclusion, the effect of this on the financial statements is to reduce the

annual depreciation charge from N16million to N8million. At the end of the

year the carrying amount of the asset would be (N48m – N8m) N40million.

All other things being equal a higher profit would be reported in the current year but would be much lower than it would have been if the assistant

accountant’s suggestion was followed.