Question

Answer

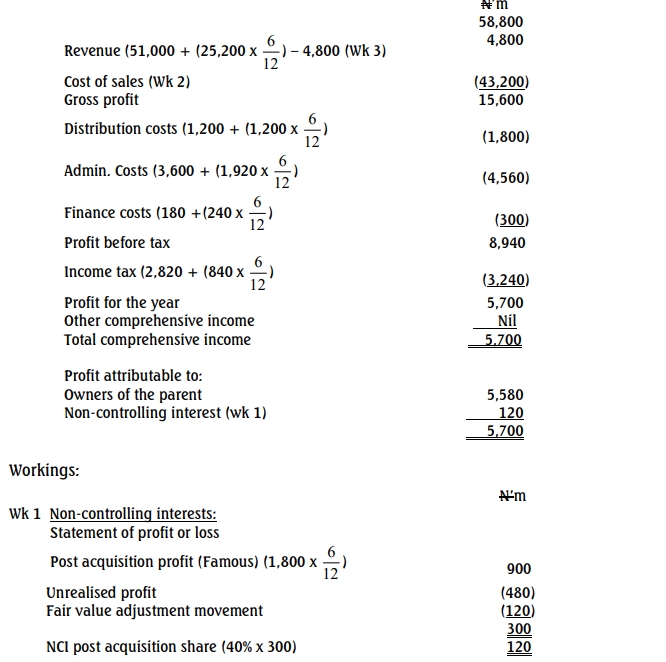

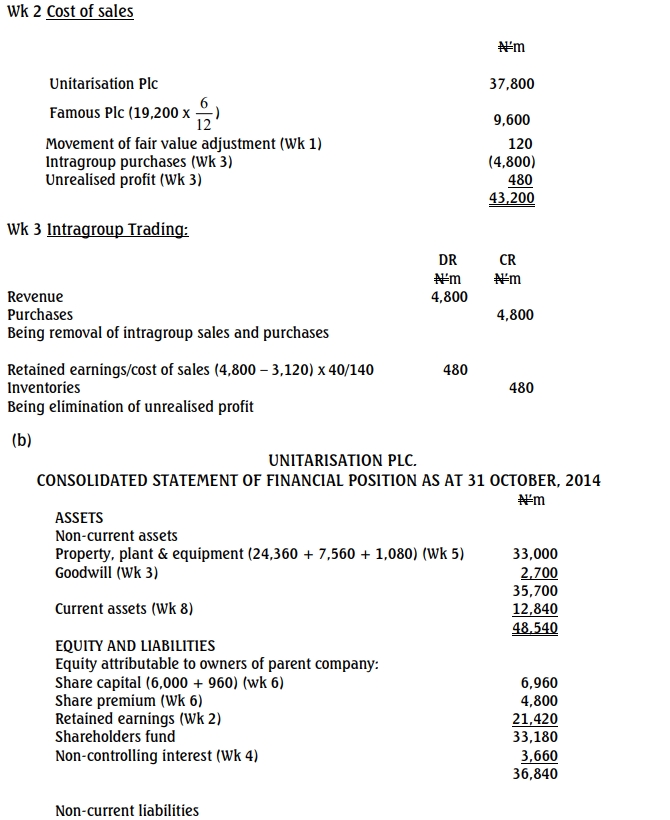

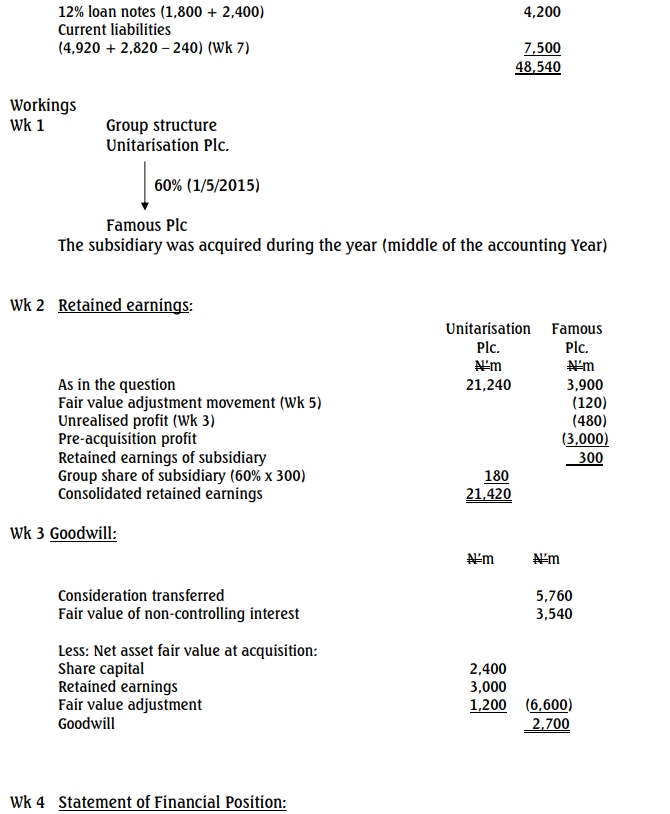

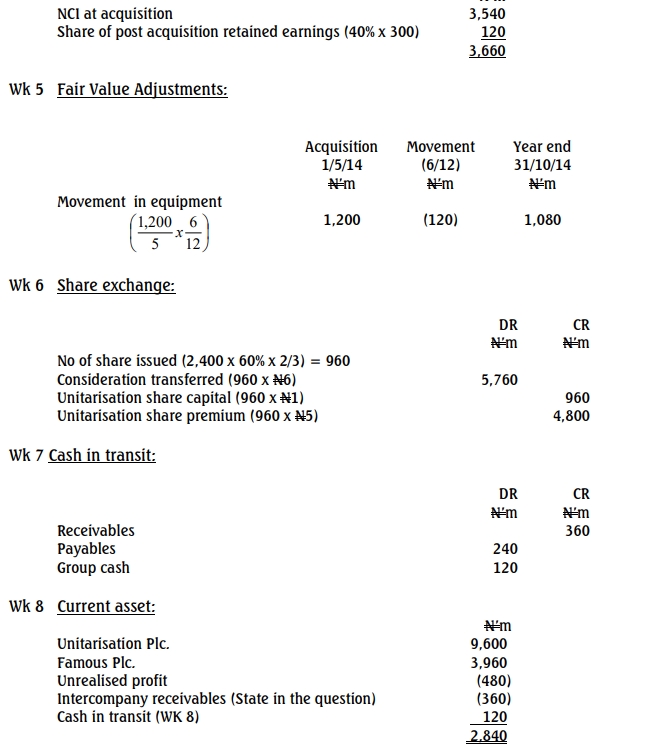

(a) Unitarisation Plc Consolidated Profit or Loss and Other Comprehensive Income for the year ended 31 October 2014

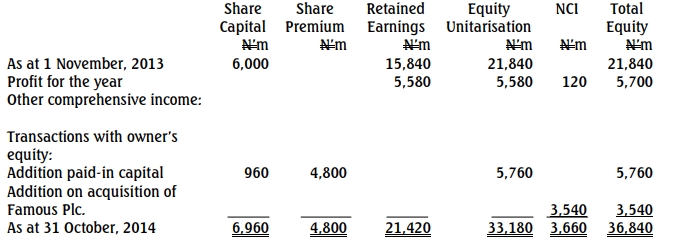

(c) Consolidated Statement of Changes in Equity for the year ended 31 October 2014

(d) Explanation of Gain on Bargain Purchase

Gain on Bargain Purchase arises when the sum of consideration transferred, non-controlling interest, and fair value of any previously held equity interest is less than the net identifiable assets acquired at the acquisition date, creating an immediate gain recognized in profit or loss.