Question

Answer

Response to Board Members:

Director A:

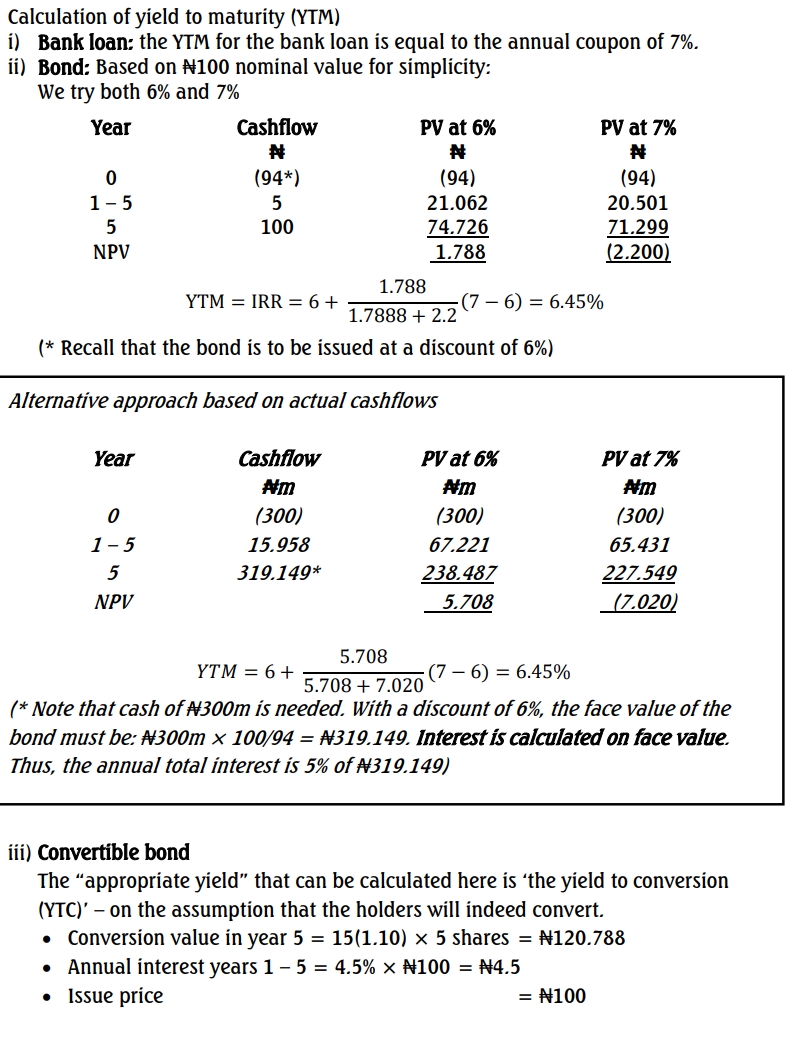

- The redemption yield (YTM) is a useful metric for comparing the cost of the loan and bond on the same basis.

- YTM is the internal rate of return (IRR) of the cash flows under a debt instrument, accounting for the time value of money.

- The unsecured bond is slightly cheaper than the loan, with a redemption yield of 6.45% compared to the bank loan’s fixed rate of 7%.

- This difference is expected, as the bond is marketed to a wider investor base, enabling finer rates.

- However, bond issuance typically incurs higher costs due to the required publicity and underwriting, which must also be considered.

Director B:

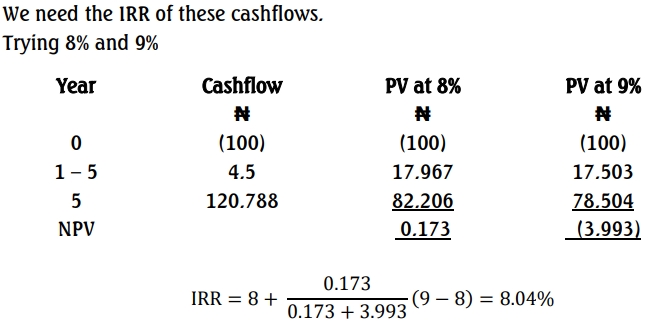

- Considering the coupon rate alone, the convertible bond appears cheaper than the unsecured bond due to its lower interest cost.

- If the share price grows as projected (10% annually), the convertible bond will convert to shares worth ₦120.80 after five years, implying a capital gain of ₦20.80 per ₦100 nominal. This represents an annualized yield of 3.85%.

- Combined with the 4.5% coupon, the overall yield of the convertible bond is 8.04%.

- Compared to the unsecured bond and bank loan, the convertible bond is the most expensive option.

- Additionally, after conversion, the company will likely incur dividend payments on the new shares, increasing its cost of capital as equity financing generally has a higher cost than debt.

Director C:

- Current investor hesitancy, highlighted by the institutional shareholders’ unwillingness to invest further, suggests market concerns about Effe’s growth potential.

- A convertible bond offers flexibility for investors, allowing them to opt for conversion into equity only if the company performs well over the next five years.

- The company benefits from lower financing costs during the bond’s term and the potential to boost its equity base post-conversion, aligning with growth and performance improvements.

Recommendation:

For a rapidly expanding entity like Effe, the convertible bond is the most appropriate financing option. It offers low-cost finance for five years, provides investors with the flexibility to convert to equity if the company performs well, and supports the company’s goal of increasing its equity base by the end of the bond period.

Workings

b) In assessing creditworthiness, a prospective investor should be provided with the following information:

• Financial statements for the last three years;

• Cash flow forecasts;

• Long- and short-term ratings from rating agencies of this and similar entities’ bonds;

• Business prospects;

• Prospects for the market sector and undertake the following analyses:

• Calculate ratios (gearing, interest cover, dividend cover, working capital ratios);

• Analyse free cash flow; and

• Carry out a risk assessment of the business and the market sector.