Question

Answer

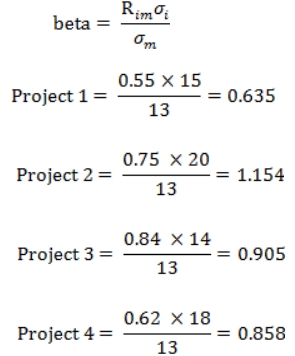

a) The beta value of each of the four projects may be estimated using:

Correlation coefficient of the project (Rim) and the market multiplied by the standard deviation of the project’s returns (i ), and all divided by the standard deviation of returns from the market (m).

The overall company beta is the weighted average of the project betas, the weighting being by their proportion of total market value. The beta of TK is estimated to be: (0.28 × 0.635) + (0.17 × 1.154) + (0.31 × 0.905) + (0.24 × 0.858) = 0.860

Using the capital asset pricing model, the return that might be expected from TK may be estimated to be: 5% + (14% – 5%) 0.860 = 12.74%

The return historically has been: (0.28 × 10%) + (0.17 × 18%) + (0.31 × 15%) + (0.24 × 13%) = 13.63%

Assuming these historic returns are expected to continue, the share price of TK is likely to be undervalued, as the company is yielding a higher return than expected for its systematic risk.

b. Why Results Might Not Identify True Share Valuation

- Assumption of Historical Continuity:

- The CAPM calculation assumes that historical risk and return patterns will persist, which might not hold true in a dynamic market.

- Limited Data:

- Using only the last five years of data may not capture long-term market trends or significant changes in risk.

- Simplified Correlation:

- The analysis uses correlation as a measure of risk but does not account for systemic shocks or unforeseen market events.

- Ignoring Non-Market Risks:

- CAPM focuses on market risk but ignores company-specific risks, such as management inefficiencies or operational issues.

- Market Efficiency Assumption:

- The CAPM model assumes markets are fully efficient, which might not reflect real-world inefficiencies in pricing or information availability.

- Risk-Free Rate and Market Return:

- These parameters are assumed constant, whereas actual risk-free rates and market returns may fluctuate due to economic conditions.

c. Limitations of Portfolio Theory in Physical Investment Decisions

- Assumption of Market Efficiency:

- Portfolio theory assumes all investors have access to the same information and that markets price assets efficiently, which might not be true for physical investment decisions.

- Simplified Risk Measures:

- Risk is quantified solely by standard deviation, ignoring qualitative factors like operational risks or regulatory changes that impact physical investments.

- Short-Term Focus:

- Portfolio theory often emphasizes short-term risk-return tradeoffs, whereas physical investments typically require a long-term perspective.

- Ignores Non-Financial Goals:

- Physical investments may aim to achieve strategic or environmental objectives, which are not considered in portfolio theory.

- Interdependencies:

- Physical investments often involve interdependent projects or assets, making the independence assumption of portfolio theory invalid.

- Inflexibility of Assumptions:

- The rigid assumptions of risk aversion, rational behavior, and consistent investor preferences limit the applicability of portfolio theory to real-world decisions.